Yes, a dismissed bankruptcy does remain on your credit report. This surprises many people who assume that because their bankruptcy case was dismissed (meaning the court rejected it or they withdrew it), the record simply disappears. It doesn’t. But the story doesn’t end there, and how you handle your credit from this point forward matters enormously، especially when understanding how judgments affect your credit and other negative marks.

What Does ‘Dismissed’ Bankruptcy Actually Mean?

A bankruptcy dismissal means the court has ended your bankruptcy case without granting you a discharge of your debts. This can happen for several reasons:

- You failed to complete required credit counseling or debtor education courses

- You missed filing deadlines or failed to submit required documentation

- You failed to make required payments in a Chapter 13 plan

- You voluntarily withdrew your petition

- The court found evidence of fraud or abuse of the bankruptcy system

A dismissal is meaningfully different from a discharge. With a discharge, your qualifying debts are legally eliminated. With a dismissal, your debts remain fully intact، and so does the bankruptcy filing on your credit report.

Dismissed vs. Discharged Bankruptcy: Key Differences

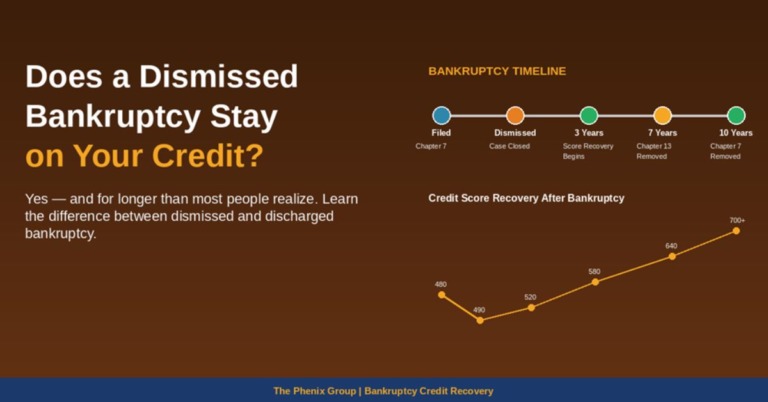

- Dismissed: Case ended, debts NOT eliminated, bankruptcy still on credit report for up to 7 years

- Discharged (Chapter 7): Debts eliminated, remains on report for 10 years from filing

- Discharged (Chapter 13): Debts partially repaid through plan, remains for 7 years from filing

- Credit Impact: Both dismissed and discharged bankruptcies significantly lower your score، but a discharge at least provides debt relief

Credit Impact: Both dismissed and discharged bankruptcies significantly lower your score, but a discharge at least provides debt relief. If you’re also trying to remove derogatory items, addressing all negative entries – not just bankruptcy – is important.

How Long Does a Dismissed Bankruptcy Stay on Your Credit Report?

A dismissed bankruptcy typically remains on your credit report for 7 years from the filing date. This applies regardless of whether the dismissal was voluntary or court-ordered. After 7 years, it must be removed under the Fair Credit Reporting Act.

If you see a dismissed bankruptcy on your report that is past the 7-year mark, you have the right to dispute it with each credit bureau and demand removal.

Can You Buy a Home After a Dismissed Bankruptcy?

Yes, but timing matters. Lenders treat dismissed bankruptcy differently than discharged bankruptcy. Since your debts were not eliminated, lenders may view you as a higher risk because you still carry the original debt load. Waiting periods vary by loan type:

- FHA Loans: Generally 1–2 years after dismissal, depending on circumstances

- Conventional Loans: Typically 2–4 years after a bankruptcy filing

- VA Loans: Generally 2 years after dismissal

Working with a credit repair specialist during this waiting period is critical. The stronger your credit file looks when you apply, the better your terms. Read our guide on credit repair Odessa TX for a detailed homebuyer credit roadmap.

If you’re wondering whether professional help is worth considering, many consumers also ask do credit repair services work when trying to recover after bankruptcy.

Frequently Asked Questions

Q: Is a dismissed bankruptcy worse than a discharged bankruptcy?:

A: From a credit score perspective, both types cause similar initial damage. However, a discharge eliminates your debt burden while a dismissal leaves your debts intact، so financially, a discharge is generally the better outcome even though both appear on your credit report.

Q: Can I refile for bankruptcy after a dismissal?:

A: Yes, in most cases. However, if your previous case was dismissed within the past 180 days for failure to comply with court orders or if you voluntarily dismissed it after a creditor sought relief from the automatic stay, refiling restrictions may apply.

Q: Can errors in bankruptcy reporting be disputed?:

A: Absolutely. If the bankruptcy is being reported inaccurately, wrong filing date, wrong type, already past the reporting window, you have every right to dispute it. The Phenix Group specializes in identifying and challenging inaccurate bankruptcy reporting.