A derogatory mark on your credit report can cost you thousands in higher interest rates, block mortgage approvals, and follow you for up to seven years. But here’s what most people don’t know: not every derogatory item is permanent, and many can be removed, sometimes even before the seven-year reporting window expires. This guide walks you through every proven method, step by step.

What Are Derogatory Items on a Credit Report?

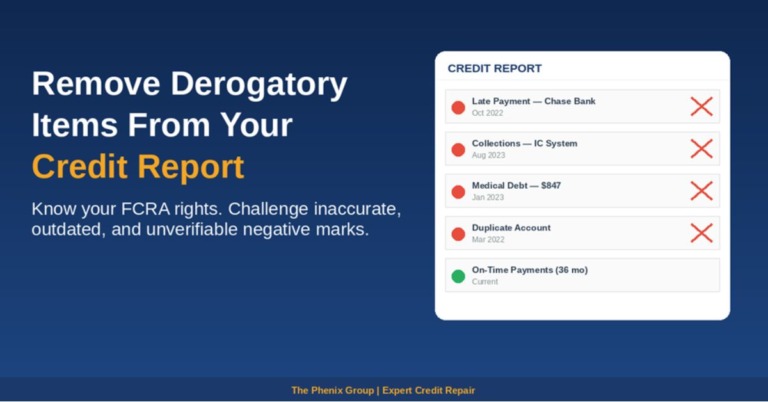

Derogatory items are negative marks that indicate you’ve failed to meet a financial obligation as agreed. Credit bureaus, Experian, Equifax, and TransUnion, record these events and they lower your credit score, sometimes dramatically. Common derogatory items include:

- Late payments (30, 60, or 90+ days past due)

- Charge-offs (when a creditor writes off your debt as a loss)

- Collections (accounts sent to third-party debt collectors)

- Bankruptcies (Chapter 7 or Chapter 13)

- Foreclosures and repossessions

- Civil judgments (in some cases, learn more about judgments on credit

- Tax liens (though these were removed from credit reports in 2018)

The impact of these items depends on their severity, recency, and how many you have. A single 30-day late payment from five years ago affects your score far less than a recent charge-off or active collection.

Common Types of Derogatory Items That Can Be Disputed

Not all negative items are created equal. Some are easier to challenge than others, especially when errors or incomplete data are involved.

Collection accounts are one of the most commonly disputed items. For example, if you’re dealing with IC System collections or HRRG Healthcare Revenue Recovery, validation and procedural disputes can be very effective.

Similarly, strategies like Caine and Weiner pay for delete can sometimes result in full removal if negotiated correctly.

How Long Do Derogatory Marks Stay on Your Credit?

- Late Payments: 7 years from the original delinquency date

- Collections: 7 years from the date of first delinquency with the original creditor

- Charge-offs: 7 years from the date of charge-off

- Chapter 7 Bankruptcy: 10 years from filing date

- Chapter 13 Bankruptcy: 7 years from filing date

- Dismissed Bankruptcy: Typically 7 years (see our guide on dismissed bankruptcy and your credit)

- Civil Judgments: No longer appear on credit reports (removed industry-wide in 2018)

Can You Remove Accurate Derogatory Items?

This is the most common question and the honest answer is: sometimes. Accurate, verifiable derogatory items cannot be legally removed through a standard dispute. However, there are legitimate paths:

- Goodwill Deletions: A written request to a creditor asking them to remove a mark as a gesture of goodwill, works best if you have an otherwise solid payment history.

- Pay for Delete Agreements: Some collection agencies (though not all) will agree to remove a collection from your report in exchange for payment. We break down specific collectors like IC System, HRRG, and Caine and Weiner in separate guides (see internal links).

- Statute of Limitations Disputes: If an item is past its legal reporting window, you can demand removal.

- Procedural Disputes: Even for accurate items, if the creditor or bureau cannot verify the information within 30 days per FCRA requirements, it must be removed.

Step-by-Step: How to Dispute Derogatory Items

- Step 1: Order your free credit reports at AnnualCreditReport.com (you’re entitled to one per bureau per year, more often after 2020 reforms).

- Step 2: Identify every derogatory item, noting the account name, date, amount, and which bureaus report it.

- Step 3: Gather supporting documentation, bank statements, payment confirmations, correspondence with creditors.

- Step 4: File a dispute online, by mail, or by phone with each bureau where the error appears.

- Step 5: Dispute directly with the original creditor if the bureau’s investigation doesn’t resolve it.

- Step 6: File a CFPB complaint at ConsumerFinance.gov if bureaus or creditors fail to respond appropriately.

- Step 7: If the dispute is rejected unfairly, consider working with a professional credit repair service that understands FCRA enforcement.

The Goodwill Letter Strategy: When and How to Use It

A goodwill letter is a personal, honest appeal to a creditor or collection agency asking them to remove a negative mark as an act of goodwill. This works best when:

- You have a long, otherwise positive history with the creditor

- The late payment was caused by a one-time hardship (medical emergency, job loss, COVID-related disruption)

- You’ve already paid the account in full

Your letter should be brief, honest, and human. Acknowledge the mistake, explain the circumstances, highlight your improved payment history, and make a specific ask. Avoid templates, creditors can spot them, and personalized letters perform far better.

When to Hire a Professional Credit Repair Service

DIY credit repair is effective for clear-cut errors, but many situations benefit from professional expertise. You should consider a professional service when:

- You have multiple derogatory items across more than one bureau

- Your disputes have been rejected without satisfactory explanation

- You’re preparing for a major purchase (home, auto) with a tight timeline

- Collections agencies are contacting you in ways that may violate the FDCPA

If you’re unsure whether it’s worth it, read this detailed guide on credit repair services.

Also, be cautious, any company that guarantees deletion of accurate items may be violating the Credit Repair Organization Act. Learn your rights here: Credit Repair Organization Act.

Frequently Asked Questions

Q: Does paying off a derogatory account remove it from my credit report?:

A: Not automatically. Paying a collection or charge-off marks it as ‘paid’ but does not erase it. The negative mark typically remains for the full 7-year window unless you negotiate a pay-for-delete agreement beforehand.

Q: Can a credit repair company remove accurate derogatory items?:

A: Reputable companies like The Phenix Group challenge items through legal and procedural means, they don’t make promises about removing verified, accurate items. Any company that guarantees removal of accurate negatives is likely making claims that violate the Credit Repair Organization Act.

Q: How many dispute letters can I send?:

A: You can dispute any item as many times as needed, but bureaus may deem repeat disputes ‘frivolous’ if there’s no new information. Vary your approach and include new evidence each time for best results.

Q: What if a collection agency bought my old debt?:

A: Third-party collectors must verify the debt upon request. If they cannot provide validation, the item must be removed. Specific collector-removal strategies vary, check our guides on IC System, HRRG, and Caine and Weiner.