Getting a call from ARS National Services, or finding their name on your credit report, can feel alarming and confusing. Most people have never heard of them, and that unfamiliarity makes it easy to assume the worst.

Here is what you need to know upfront: ARS National Services is a real, legitimate debt collection agency. It is not a scam. However, that does not automatically mean the debt they are pursuing is valid, accurately reported, or something you are legally obligated to pay.

This guide breaks down exactly who ARS National Services is, why they are contacting you, how their collections affect your credit, and, most importantly, what your rights are and what you can do about it. If you want to go straight to the removal process, you can read our complete guide to removing ARS collections from your credit report for a more in-depth look at each strategy.

What Is ARS National Services?

ARS National Services is a third-party debt collection agency headquartered in Escondido, California. Founded in 1987, ARS has grown into one of the largest consumer debt collection operations in the United States, operating in all 50 states with regional offices in California, Florida, and Texas. The company holds an A+ rating with the Better Business Bureau and has been BBB-accredited since 2011.

ARS operates under two main business models. In some cases, it purchases charged-off accounts directly from original creditors, paying pennies on the dollar for the right to collect the balance. In other cases, ARS is hired by an original creditor on a contingency basis, collecting on their behalf for a percentage of what it recovers. Either way, the result for you as a consumer is the same: ARS is now contacting you and may be reporting to your credit bureaus.

Despite its relatively clean regulatory standing, ARS has accumulated a substantial number of consumer complaints with the Consumer Financial Protection Bureau (CFPB) and federal lawsuits alleging violations of the Fair Debt Collection Practices Act (FDCPA). Knowing this matters, because a documented FDCPA violation can give you legal leverage to have the account removed from your credit report and potentially recover damages.

Who Does ARS National Services Collect For?

ARS National Services primarily collects on behalf of financial services organizations, including major banks and credit card companies. Its known clients include institutions such as Citibank, Chase, Capital One, and Bank of America, among others. Beyond financial services, ARS also collects for a broad range of industries, including:

- Healthcare providers and hospitals

- Auto loan lenders

- Retail credit card issuers

- Consumer loan companies

- Marketplace and fintech lenders

- Student loan servicers

- Utility providers and telecom companies

This wide client base means that if you have any unpaid account in any of these categories, ARS may have been hired or purchased the debt to pursue collection.

ARS National Services Phone Numbers to Watch For

One of the most common questions people ask is whether a call from an unfamiliar number is actually ARS National Services or a scam impersonating them. ARS uses multiple phone numbers to contact consumers. Known numbers associated with ARS National Services include:

- (800) 456-5053

- (800) 245-2867

- (800) 440-6613

- (866) 888-9096

- (800) 665-3140

If you receive a call from any of these numbers, it is likely ARS. Do not provide payment information over the phone until you have verified the debt in writing.

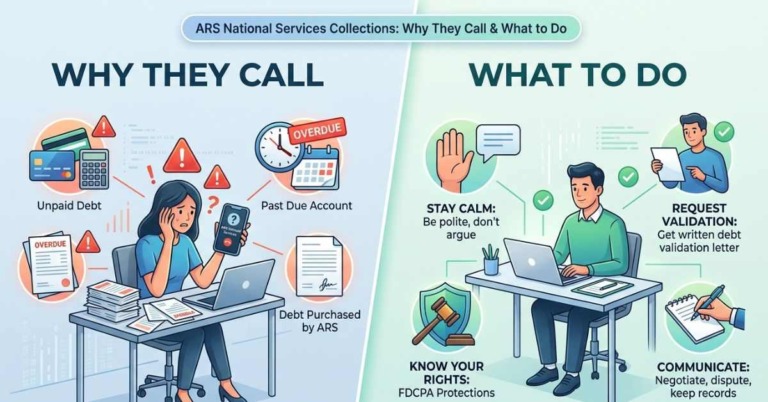

Why Is ARS National Services Calling Me?

If ARS National Services is calling you, there are two primary reasons.

You Have an Unpaid Debt with One of Their Clients

The most common reason is that you have an account that became delinquent, typically after going unpaid for 90 to 180 days, and the original creditor either sold the debt to ARS or hired them to collect it. ARS may call you repeatedly, send letters, and in some cases, make in-person contact in an attempt to collect the balance.

Ignoring these calls is almost never the right move. Even if you dispute the debt, going silent can allow ARS to continue reporting the account to the three major credit bureaus, Equifax, Experian, and TransUnion, where it will damage your credit score for years.

ARS May Be Calling About a Debt You Don’t Actually Owe

This is more common than most people realize. ARS, like all debt collectors, sometimes pursues consumers for debts that:

- Were already paid and are being collected again in error

- Belong to someone else with a similar name or Social Security Number

- Are past the statute of limitations and legally uncollectable

- Were previously discharged in bankruptcy

- Were reported with incorrect amounts or incorrect account information

According to a study by the U.S. PIRG (Public Interest Research Group), approximately 79 percent of credit reports contain errors. That means that even if ARS is calling you, the debt they are pursuing may not be valid or accurately reported. This is why verifying the debt before taking any action, especially before making payment, is essential.

How ARS National Services Collections Damages Your Credit Score

A collection account from ARS National Services is one of the most damaging items that can appear on your credit report. A single collection entry can lower your credit score by 50 to 100 points or more, depending on your credit history and the scoring model being used.

The damage is even more severe under traditional FICO scoring models, the models most commonly used by mortgage lenders. Even after a collection account is paid, it continues to appear on your report as a “paid collection,” which many lenders still treat as a red flag when reviewing mortgage applications or loan requests.

The account will remain on your credit report for seven years from the original date of delinquency, meaning the date the account first went past due with the original creditor, regardless of when ARS purchased or was assigned the debt. This timeline does not reset if you make a partial payment or speak with the collector on the phone, though making an actual payment can restart the statute of limitations in some states.

The critical implication of all of this: paying ARS does not automatically remove the account from your credit report or meaningfully improve your score. The entry remains, just with a status change from “unpaid collection” to “paid collection.” For many consumers, particularly those applying for a mortgage, this distinction matters very little to lenders.

Your Legal Rights When Dealing with ARS National Services

Federal law gives you significant protections when dealing with any debt collector, including ARS. Understanding these rights is not just useful, it is the foundation of every effective strategy for handling a collection account. For a deeper look at these protections, read our article on what the FDCPA allows and prohibits.

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA is the primary federal law governing third-party debt collectors. Under this law, ARS National Services is prohibited from:

- Calling you before 8:00 AM or after 9:00 PM in your time zone

- Using abusive, obscene, or threatening language

- Threatening to sue you when they have no intention of filing a lawsuit

- Telling your employer, neighbors, or other third parties that you owe a debt

- Misrepresenting themselves as government officials, law enforcement, or attorneys

- Adding unauthorized fees or interest to the debt amount

- Contacting you at work after you have told them your employer disapproves

If ARS violates any of these rules, you have the right to sue them in federal or state court. Successful FDCPA claims can result in damages of up to $1,000 per violation, plus attorney’s fees, and the collector pays your legal costs if you win. Documented FDCPA violations also frequently serve as grounds for credit bureaus to delete the associated account from your report.

The Fair Credit Reporting Act (FCRA)

The FCRA governs how debt collectors report information to credit bureaus. Under the FCRA, you have the right to:

- Dispute any information on your credit report that is inaccurate, incomplete, or unverifiable

- Require ARS and the credit bureaus to investigate your dispute within 30 days

- Have inaccurate or unverifiable information deleted from your report

If ARS cannot verify the accuracy of what they are reporting, the credit bureaus are required to remove the account, regardless of whether you owe the underlying debt.

The Telephone Consumer Protection Act (TCPA)

The TCPA specifically protects you from robocalls and auto-dialed calls. If ARS is calling you using an automated dialing system or pre-recorded messages without your prior express consent, you may be entitled to $500 per violation, and up to $1,500 per violation if the conduct was willful. Many ARS complaints include allegations of exactly this type of automated calling.

Should You Pay ARS National Services? (Read This First)

This is the most consequential decision you will make in this process, and the wrong move can lock a negative account in place on your credit report for years.

Do not pay ARS before doing these things:

1. Verify the debt is valid. Request written debt validation before taking any other action. ARS is legally required to provide documentation proving the debt is yours, the amount is accurate, and they have the legal right to collect it. If they cannot validate, they must stop collection activity.

2. Check the statute of limitations. Every state has a statute of limitations that limits the time a collector can sue you to collect a debt. In many states, this ranges from three to six years from the date of the last payment. If the debt is time-barred, making even a small payment can restart the clock and revive the collector’s ability to sue you.

3. Understand that paying may not help your credit. As noted above, a paid collection still appears on your report for seven years. Under the older FICO scoring models used by most mortgage lenders, a paid collection is still a negative mark. The only payment arrangement that meaningfully improves your credit is a pay-for-delete agreement, where ARS agrees in writing to completely remove the account from your credit report in exchange for payment.

4. Consider the mortgage timeline. If you are planning to buy a home or refinance, the strategy for handling an ARS collection is more nuanced than simply paying or ignoring it. Some loan programs have specific requirements around outstanding collections, and the wrong approach can delay or derail your approval. If homeownership is your goal, connect with the credit repair specialists at The Phenix Group before taking any action, our analysts are uniquely experienced in mortgage-driven credit restoration.

How to Remove ARS National Services from Your Credit Report

Removing ARS from your credit report is achievable, but it requires a methodical approach and careful documentation. Here are the five strategies, in order of preference.

Step 1: Pull Your Three-Bureau Credit Report

Before you do anything else, pull your full credit reports from all three bureaus, Equifax, Experian, and TransUnion, at AnnualCreditReport.com. ARS may be reporting to one bureau and not others, or reporting different balances across bureaus.

Review each report for:

- Incorrect account numbers or balances

- Wrong dates of first delinquency (this affects how long the account stays on your report)

- Accounts that are too old to legally remain on your report (older than 7 years)

- Accounts that are not yours

- Duplicate entries for the same debt

Document every discrepancy. These are your dispute grounds.

Step 2: Send a Debt Validation Letter Within 30 Days

Under the FDCPA, you have 30 days from first contact with ARS to request debt validation in writing. This letter formally demands that ARS prove:

- The debt is yours

- The amount is accurate and current

- They have the legal right to collect it

- The name and address of the original creditor

Send the letter via certified mail with return receipt requested, this creates a paper trail. If ARS cannot validate the debt, they must cease collection activity and cannot continue reporting the account to the credit bureaus.

Step 3: Dispute Inaccurate Information with the Credit Bureaus

If you identify inaccuracies, wrong dates, wrong balances, wrong account status, submit a formal dispute to each credit bureau reporting the account. Include all supporting documentation. The bureau has 30 days to investigate, contact ARS, and either confirm or delete the account. If ARS cannot confirm the accuracy within that window, the account must be removed.

Step 4: Negotiate a Pay-for-Delete Agreement

If the debt is valid and you choose to pay, negotiate a pay-for-delete agreement before sending a single dollar. This means ARS agrees in writing to completely delete the account from your credit report, not just mark it as paid, in exchange for your payment. Get the agreement on The Phenix Group letterhead if working with a professional, or at minimum via written correspondence on ARS letterhead before you pay anything.

Note: Pay-for-delete is less common with large collectors than with smaller agencies, but it is negotiable, especially if you are offering a lump-sum payment or settling for less than the full amount owed.

Step 5: File a CFPB Complaint if Your Rights Are Violated

If ARS has violated the FDCPA, FCRA, or TCPA, file a formal complaint with the Consumer Financial Protection Bureau at consumerfinance.gov/complaint. The CFPB forwards your complaint to ARS and requires a response. Documented violations can also serve as grounds to have the account deleted by the credit bureaus. You may also have grounds to file a state attorney general complaint or a federal lawsuit.

How ARS Collections Affects Your Mortgage Eligibility

This is a topic no competitor addresses, and it is the angle that matters most to The Phenix Group’s core audience.

If you are working toward homeownership or a mortgage refinance, an ARS collection account can create serious obstacles. Mortgage underwriting guidelines vary by loan type, but the general impact is significant:

- Conventional loans: Most lenders require collection accounts to be resolved before closing, particularly for amounts over $2,000

- FHA loans: While FHA does not automatically require payment of collection accounts, they are still factored into debt-to-income ratio calculations

- VA and USDA loans: Similar considerations apply

Even more importantly, most mortgage lenders still use FICO 2, 4, and 5 scoring models, older versions that do not reduce the impact of paid collections the way FICO 9 does. This means even a paid ARS collection can still suppress your score enough to disqualify you from preferred interest rates.

The Phenix Group’s credit repair program is specifically designed around mortgage timelines. We work directly with your lender to ensure the dispute process aligns with your closing date. If you are buying a home, do not attempt to resolve ARS on your own without first understanding how it affects your loan program. Reach out to our team for a free credit analysis before making any decisions.

Why Professional Credit Repair Gets Faster Results

The steps outlined above are available to any consumer. But successfully executing them, with the right documentation, in the right sequence, within the right legal deadlines, is where most people make costly mistakes.

Common DIY errors include:

- Making a payment before validating the debt (potentially restarting the statute of limitations)

- Disputing without sufficient documentation (resulting in “verified” status that is harder to challenge again)

- Missing the 30-day validation window

- Accepting a verbal pay-for-delete promise without written confirmation

- Disputing the same account repeatedly without new grounds (which credit bureaus may classify as frivolous)

If you want to understand more about where DIY efforts go wrong, read our detailed guide on why DIY credit repair often fails and when professional help makes sense.

The Phenix Group brings an attorney-engaged process to every client case. Our analysts do not just file generic dispute letters, we analyze the legal and reporting accuracy of every account, engage directly with collectors and original creditors, and pursue removal through every available channel simultaneously. This is why lenders, real estate agents, and mortgage professionals nationwide refer their clients to us when credit issues threaten to delay a closing.

We have helped consumers remove CCS collections, Jefferson Capital accounts, Southwest Credit Systems, Penn Credit entries, and dozens of other major collection agencies, and ARS National Services is no different.

Frequently Asked Questions

Is ARS National Services a scam?

No. ARS National Services is a legitimate, licensed debt collection agency founded in 1987 and headquartered in Escondido, California. It is accredited by the Better Business Bureau with an A+ rating and operates in all 50 states. However, a legitimate company can still use aggressive or illegal collection tactics. Always verify any debt they claim you owe before taking action.

Why is ARS National Services calling me when I don’t recognize the debt?

ARS may be calling about a debt from an original creditor you have forgotten, a debt that has been sold multiple times and reported under a different account name, a debt that belongs to someone else, or an error. Request debt validation in writing before discussing the account.

How long does ARS National Services stay on my credit report?

A collection account from ARS can remain on your credit report for up to seven years from the original date of delinquency with the first creditor. This clock does not reset if the debt is sold to ARS or if you make a payment, though payment can restart the statute of limitations for legal action in some states.

Should I pay ARS National Services?

Not necessarily, and not without a strategy. Paying does not automatically remove the account from your credit report. A paid collection still damages your credit score under most lending models. If you decide to pay, negotiate a pay-for-delete agreement in writing first. Better yet, consult with a credit repair professional before paying anything to understand all your options.

Can ARS National Services sue me?

Yes, though it is not their primary collection strategy. ARS can file a lawsuit if the debt is still within your state’s statute of limitations. If they obtain a judgment against you, they may be able to garnish your wages or place a lien on assets, depending on your state’s laws. If you receive a summons, respond to it, do not ignore a lawsuit.

How do I stop ARS National Services from calling me?

Under the FDCPA, you can send ARS a written cease-and-desist letter demanding they stop calling you. Once received, they may only contact you to confirm they will stop, or to notify you of a specific action they intend to take (such as filing a lawsuit). Send it via certified mail. Note that stopping calls does not eliminate the debt or the credit reporting.

What is a debt validation letter and should I send one to ARS?

A debt validation letter is a formal written request demanding that ARS prove the debt is valid and belongs to you. Under the FDCPA, you have 30 days from first contact to send this request. ARS must respond with documentation before continuing collection activity. It is one of the most powerful tools available to consumers.

Does ARS National Services do pay-for-delete?

Pay-for-delete is not guaranteed with ARS, but it is negotiable, especially for older debts or when offering a lump-sum settlement. Always get any pay-for-delete agreement in writing before making payment. A professional credit repair service can significantly improve your odds of securing this outcome.

Ready to Get ARS National Services Off Your Credit Report?

An ARS National Services collection does not have to follow you for seven years. With the right strategy, and the right team, removal is a real, achievable outcome.

The Phenix Group is trusted by homebuyers, mortgage lenders, loan officers, and real estate professionals nationwide. Our attorney-engaged credit restoration process goes beyond generic bureau disputes. We engage directly with collectors and creditors, analyze reporting inaccuracies, pursue FDCPA and FCRA violations, and do everything possible to remove damaging accounts permanently.

Here is what working with us looks like:

- Free credit analysis to identify every removal opportunity

- Attorney-engaged dispute process, not just generic letters

- Direct creditor and collector engagement

- Mortgage-timeline alignment with your lender

- Nationwide service with local expertise in Fort Worth, Dallas, Austin, and beyond

Do not let ARS National Services damage your credit and your financial future. Get your free credit analysis from The Phenix Group today and take back control.

This blog is for informational purposes only and is not legal advice. Natasha George is President of The Phenix Group, a licensed Mortgage Loan Originator and credit professional with over two decades of industry experience. She holds an MBA from Texas Christian University.