Caine and Weiner does not have a formal pay-for-delete policy, but consumers have successfully negotiated deletions, particularly on smaller balances and accounts with questionable documentation. Similar strategies used with IC System pay for delete cases can sometimes apply here as well. Here’s how to approach it strategically.

Who Is Caine and Weiner?

Caine and Weiner (also known as Caine & Weiner Company, Inc.) is a debt collection agency that has been operating since 1930, making them one of the oldest collection firms in the United States. They collect on behalf of various industries including:

- Financial services and banks

- Healthcare organizations, including accounts that may resemble HRRG collections

- Retail and commercial creditors

- Government agencies

They are a legitimate, licensed collection agency, but like all debt collectors, they are subject to the Fair Debt Collection Practices Act (FDCPA) and must follow specific rules around how they pursue and report debts.

Caine and Weiner’s Pay for Delete Policy in Practice

Officially, most major collection agencies including Caine and Weiner will tell you they don’t offer pay-for-delete. Their standard position is to update the account to ‘paid in full’ or ‘settled’ – which still leaves the negative mark on your report for the full 7-year window.

However, in practice, negotiation is possible, especially when:

- The debt balance is under $1,000 (smaller balances are easier to leverage)

- The account is difficult to verify (documentation gaps work in your favor and may help you remove derogatory items

- You communicate professionally in writing, not by phone

- You frame the request as a ‘mutual benefit’ settlement, not a demand

If negotiations fail, some consumers also explore professional credit repair services to challenge inaccurate reporting.

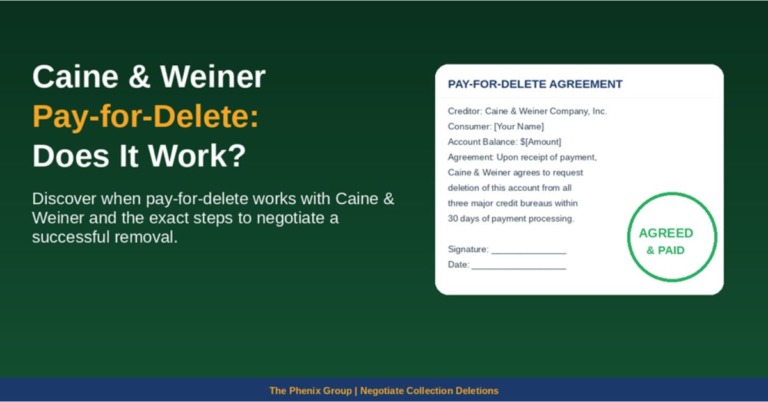

How to Send a Pay for Delete Request to Caine and Weiner

Your letter should accomplish three things: offer payment, request deletion, and specify the terms. Key elements to include:

- Your full name, address, and the account number in question

- The exact settlement amount you’re offering (typically 25–60% of the balance)

- A clear request for written confirmation of deletion from all three bureaus

- A deadline for their response (10–14 business days is reasonable)

- A statement that you will only pay upon receipt of a signed written agreement

Do not call. Everything with collection agencies should be in writing, sent via certified mail with return receipt requested.

Frequently Asked Questions

Q: Can Caine and Weiner take me to court?:

A: Yes, but they typically pursue legal action only on larger balances where the cost of litigation is justified. Check your state’s statute of limitations on debt, if the debt is old, they may not be able to sue.

Q: What if Caine and Weiner can’t verify my debt?:

A: Under the FDCPA, if they cannot provide adequate validation of the debt within 30 days of your request, they must cease collection activity and the item should be removed from your credit report.

Q: What happens if I ignore Caine and Weiner?:

A: Ignoring a legitimate collection account doesn’t make it go away. It stays on your credit report for 7 years, continues to lower your score, and they may pursue further collection action or litigation. It’s always better to address the account proactively.