Seeing a collection account on your credit report can feel like a financial landmine, one that quietly ruins your chances of getting a mortgage, a car loan, or a new apartment. If you’ve been asking ‘how to get creditor to remove collection,’ you’re not alone. Millions of Americans face this exact situation every year.

The good news: you have more options than most people realize. There are five legitimate, proven methods for getting a creditor to remove a collection from your credit report, and knowing which one applies to your situation can save you months of frustration and thousands of dollars. For a broad overview, see our full guide on removing collections from your credit report.

In this guide, we’ll walk through every strategy step by step, cover your legal rights under the FDCPA and FCRA, and explain exactly when professional help is worth it.

What Is a Collection Account and Why Does It Damage Your Credit?

A collection account is created when you fail to repay a debt and the original creditor, a bank, medical provider, utility company, or lender, gives up trying to collect it themselves. They either sell your debt to a third-party collection agency at a steep discount, or hire one to recover it on their behalf.

Once the account is in collections, a new negative entry typically appears on all three of your credit reports: Equifax, Experian, and TransUnion. Payment history makes up approximately 35% of your FICO credit score – the most heavily weighted factor – which is why even a single collection account can cause a significant score drop.

Under the Fair Credit Reporting Act (FCRA), a collection account can legally remain on your credit report for up to seven years from the date the original account first became delinquent. The five strategies below are designed to get that collection removed sooner, and legally.

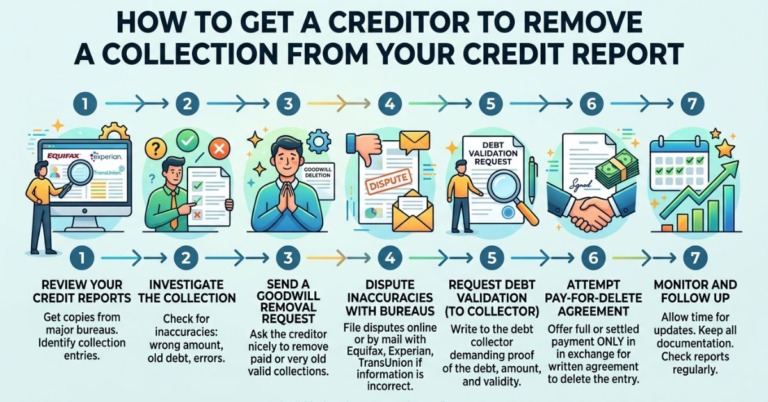

Method 1: Request a Goodwill Deletion (Best for Paid Debts)

If you’ve already paid off the collection in full, you may be able to ask the creditor or collection agency to remove it as an act of goodwill. This is called a goodwill deletion, a polite, professional written request asking them to wipe the negative account from your credit report because you’ve paid the debt and demonstrated improved financial behavior.

A goodwill deletion works best when the delinquency was an isolated incident in an otherwise clean credit history. Many creditors are more sympathetic than people expect, especially if you can explain a specific hardship, job loss, a medical emergency, or a brief financial crisis, that caused the missed payment.

What to Include in a Goodwill Deletion Letter

- Your full name, address, and account number as it appears on your credit report

- A clear statement confirming the debt has been paid in full

- A brief, honest explanation of the circumstances that caused the missed payment

- Evidence of your improved payment behavior (e.g., 12+ months of on-time payments)

- A specific, polite request to remove the collection account as a goodwill gesture

- Send via certified mail with return receipt, this creates a documented paper trail

Note: Late payment entries may still remain on your report even if the collection is removed, but eliminating the collection itself can meaningfully boost your score. Our credit repair services can help you draft and submit these letters professionally.

Method 2: Negotiate a Pay-for-Delete Agreement

A pay-for-delete agreement is when you offer to pay the collection debt, either in full or as a settlement, in exchange for the collection agency agreeing to delete the account from your credit reports. Unlike a goodwill deletion, payment is the explicit condition of removal, and the deal must be formalized in writing before you pay a single dollar.

How to Approach a Pay-for-Delete Negotiation

- Contact the collection agency in writing, never by phone, so every communication is documented.

- State clearly that you are willing to pay the balance (or negotiate a settlement) in exchange for complete deletion from all three credit bureaus.

- Get their written agreement BEFORE sending any payment. A verbal promise means nothing.

- After payment clears, monitor your credit reports within 30–45 days to confirm the account was removed.

Important Warning Before You Use Pay-for-Delete

| WARNING: Pay-for-delete sits in a legal gray zone. The FCRA requires creditors to report accurate information, and credit bureaus actively discourage the practice, many major collectors will simply refuse Critically: Making any payment on an old debt can legally RESTART the statute of limitations in your state (typically 3–6 years), potentially giving the collection agency new grounds to sue you. Never pay an old debt without first understanding the implications. This is exactly why working with an attorney-backed credit repair service can be transformational — professionals navigate these negotiations strategically. |

Method 3: Dispute Inaccurate Collection Accounts

If a collection account contains any inaccurate, incomplete, or unverifiable information, you have the legal right to dispute it under the FCRA. This is one of the most powerful tools available, and it doesn’t require paying the debt.

Common errors that warrant a dispute: wrong balance amount, incorrect account dates, an account that doesn’t belong to you (mixed file or identity issue), duplicate reporting of the same debt, or a collection from a creditor that has since gone out of business (making the debt unverifiable).

How to File a Credit Bureau Dispute (Step-by-Step)

- Pull your free credit reports from all three bureaus at AnnualCreditReport.com.

- Identify the inaccurate collection account and gather all supporting documentation.

- File a formal dispute with each bureau reporting the error (Equifax, Experian, TransUnion each have online portals).

- Alternatively, send a 609 dispute letter via certified mail requesting documentation proving the debt is yours. If the bureau or collector cannot verify the information within 30–45 days, it must be removed.

- Follow up. The bureau is required by law to notify you of the investigation results within 30–45 days.

What Happens After You File a Dispute?

The credit bureau contacts the collection agency and asks them to verify the debt. If the collector cannot provide complete, accurate documentation within the required timeframe, the bureau must delete the account. The Phenix Group handles this entire process on behalf of our clients, we engage specific collectors including CCS collections removal, original creditors, and all three bureaus simultaneously.

Method 4: Send a Debt Validation Letter

Under the Fair Debt Collection Practices Act (FDCPA), you have the legal right to demand that any collection agency prove the debt is valid and legally belongs to you. This is called debt validation. You must send your written request within 30 days of the collector’s first contact, once you do, they must cease collection activity until they provide adequate validation.

If they can’t validate the debt properly, it may be eligible for removal. To fully understand your legal rights when dealing with collectors, read our detailed guide on your rights under the FDCPA.

What Your Debt Validation Letter Must Include

- Your full name and mailing address

- The collection account number as it appears on your credit report

- A formal request for the name and address of the original creditor

- A request for the original signed agreement showing you owe this specific debt

- A request for a complete payment history and current balance breakdown

- A request for proof that the agency is licensed to collect in your state

- Send via certified mail, return receipt requested, keep a copy of everything

Method 5: Wait for the 7-Year Automatic Removal

Sometimes patience is the most strategic move. Under the FCRA, a collection account must be automatically removed from your credit report seven years from the date the original account first became delinquent, regardless of whether you paid it or not.

This approach may be the right choice when the collection is already 5–6 years old, the amount is small, or any attempt to dispute or negotiate would risk restarting the statute of limitations in your state.

What About Medical Collections?

Medical debt has received major regulatory attention in recent years. The Consumer Financial Protection Bureau (CFPB) finalized a rule to remove medical bills from credit reports, a development that could benefit tens of millions of Americans carrying medical collection accounts.

If you have medical collections on your report, this regulatory change may offer an additional removal pathway beyond the five methods above. Our credit repair team stays current on all rule changes and can advise you on how these updates apply to your specific situation. Start with a free credit analysis to find out.

When Should You Hire a Professional Credit Repair Company?

The five methods above can be pursued on your own. But many people find that DIY attempts stall – disputes get rejected, collectors ignore letters, negotiations fall apart – and weeks turn into months with no movement. There’s a real cost to waiting if a collection is blocking a mortgage approval or a car loan.

Consider working with a professional credit repair company if any of the following apply:

- You have multiple collection accounts across all three bureaus

- You’re preparing to buy a home or finance a vehicle in the next 60–90 days

- Your own dispute or goodwill attempts have been ignored or rejected

- The collection involves potential identity theft or a mixed credit file

- You’re unsure whether paying the debt would help or hurt your credit goals

The Phenix Group goes far beyond generic letter-writing. We engage directly with original creditors, finance companies, collection agencies, and all three credit bureaus simultaneously, holding them accountable under FDCPA and FCRA consumer protection law. Our process is attorney-audited, and most clients see results within 60 days. Learn more about what credit repair for home ownership looks like when a mortgage is your goal.

We serve clients nationwide, including dedicated local teams offering credit repair in Fort Worth, credit repair in Chicago, and credit repair in Los Angeles. No matter where you are, we build a personalized plan around your specific goals and timeline.

Curious about the investment? Review our transparent credit repair pricing before your consultation.

Frequently Asked Questions

Can I ask a creditor to remove a collection account?

Yes. You can request removal through a goodwill deletion letter if you’ve already paid, or negotiate a pay-for-delete agreement before payment. Creditors are not legally required to remove accurate information, but many will under the right circumstances, especially with professional guidance.

Does paying a collection automatically remove it from my credit report?

No. Paying a collection does not automatically remove it. A paid collection still appears on your report for up to seven years. You need to specifically negotiate removal, through a pay-for-delete agreement or a goodwill deletion request, to have it removed after payment.

What is a pay-for-delete agreement?

A pay-for-delete agreement is an arrangement where you offer to pay a collection debt in exchange for the agency removing the account from your credit reports. It must be agreed upon in writing before any payment is made. Note: many major collectors refuse, and this approach requires careful handling.

How long does a collection stay on my credit report?

Under the FCRA, a collection account can remain on your credit report for up to seven years from the date the original account first became delinquent, whether you’ve paid it or not. Removal strategies above can help you eliminate it before that window expires.

Can I remove a collection without paying it?

Yes, in some cases. If the collection contains inaccurate or unverifiable information, you can dispute it and have it removed without payment. A debt validation letter under the FDCPA is another tool, if the collector cannot validate the debt, it may be removed.

What is a goodwill deletion letter?

A goodwill deletion letter is a written request to a creditor or collection agency asking them to remove a paid collection account as a favor. It works best when you have an otherwise clean credit history and can explain the delinquency was caused by an isolated hardship.

What is a 609 dispute letter?

A 609 dispute letter is a formal request under Section 609 of the FCRA asking the credit bureau to provide documentation verifying a disputed item. If the bureau or collector cannot verify the information within 30–45 days, the item must be removed.

Will removing a collection improve my credit score?

Yes. Removing a collection from your credit report can significantly improve your score, especially under newer FICO and VantageScore models that don’t count paid collections. The exact improvement depends on how many other negative items remain on your report.

What if the creditor refuses to remove the collection?

If a creditor refuses to remove an inaccurate collection, escalate your dispute to the credit bureaus, file a complaint with the CFPB, or consult with a professional credit repair company. If the creditor violated FDCPA or FCRA rules, you may have grounds for legal action.

When should I hire a professional credit repair company to remove collections?

Consider hiring a professional if you have multiple collections, are preparing for a mortgage, your own attempts have failed, or you want expert guidance on the best legal strategy for your situation. The Phenix Group offers a free credit analysis to determine the right approach for you.