You finally paid off that collection account, and now you’re refreshing your credit score every day waiting for it to move. Sound familiar?

Here’s the honest truth: paying off a collection account is the right move, but the timeline for credit score improvement is more complicated than most people expect. The answer depends heavily on which credit scoring model your lender uses, how old the collection is, and what else is happening on your report.

This guide breaks down exactly what to expect, when to expect it, and how to speed up the process.

The Short Answer: Here’s Your Credit Timeline

Before diving deep, here’s the direct answer you came here for:

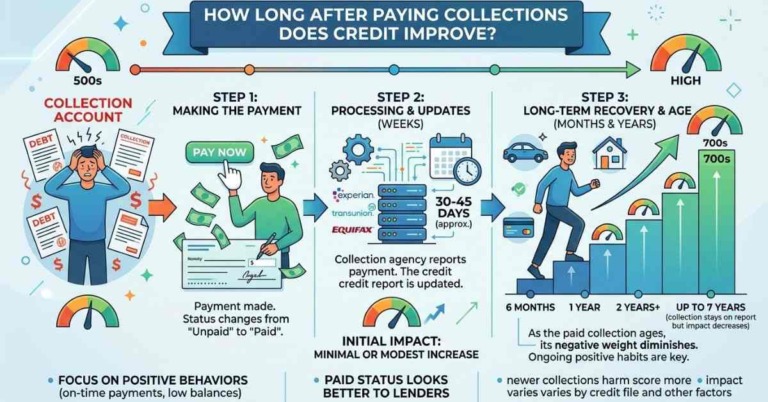

Status Update: 30–60 days after payment (once the collector reports to the bureaus)

Score Movement: Anywhere from no change to a modest improvement within 1–3 months

Meaningful Recovery: 3–12 months, depending on your overall credit profile

Full 7-Year Removal: The collection stays on your report for 7 years from the original delinquency date, paid or not

The key frustration most people run into? They expect their credit score to jump the moment they pay. But that’s not how it works.

When Will the “Paid” Status Show on My Report?

After you pay a collection, the collection agency needs to update their records and notify the three credit bureaus, Equifax, Experian, and TransUnion. This doesn’t happen instantly.

According to Experian, how long before a collection agency reports to the credit bureau depends on the collector’s reporting cycle, but it typically takes 30 to 60 days for your report to reflect “paid.” Each bureau updates on its own independent schedule, so you may see the update on one bureau before the others.

When Will My Score Actually Start Rising?

This is where most articles skip the nuance, and where understanding your situation can save you months of confusion.

How long does credit repair take is a question we get constantly at The Phenix Group. The answer for collections specifically: most clients see initial score movement within 60–90 days, but significant improvement typically unfolds over 3–12 months as you build new positive history on top of the existing negative mark.

Why Paying Collections Doesn’t Always Boost Your Score Immediately

This is the part that surprises most people: simply paying a collection account often produces little to no immediate score increase under the most widely used scoring model (FICO 8).

The reason is simple, paying doesn’t erase the history. The collection account still exists on your report, still shows the original delinquency, and still counts against your payment history. Only the status changes from “unpaid” to “paid.”

The FICO Version Problem No One Talks About

Here’s a critical nuance that most articles, and most borrowers, completely miss:

Not all FICO models treat paid collections the same way.

| Credit Scoring Model | Paid Collections | Unpaid Collections | Medical Collections |

|---|---|---|---|

| FICO Score 8 (most widely used) | Still counts against you (if over $100) | Negative impact | Negative impact |

| FICO Score 9 | Ignored, no impact | Negative impact | Lower weight than other collections |

| FICO Score 10 | Ignored, no impact | Negative impact | Lower weight than other collections |

| VantageScore 3.0 | Ignored, no impact | Negative impact | Ignored (paid or unpaid) |

| VantageScore 4.0 | Ignored, no impact | Negative impact | Ignored (paid or unpaid) |

What this means for you: If your lender uses FICO Score 8 (and many mortgage lenders do), paying off a collection may not raise your score at all, at least not directly. However, if they use FICO 9, 10, or VantageScore 4.0, paying it off could remove the negative weight entirely and give your score a real boost.

Before making any payment decisions, it’s worth asking your lender which scoring model they use, or requesting a free credit analysis from a specialist who can review your full profile.

How VantageScore Treats Paid Collections Differently

VantageScore 3.0 and 4.0, the scoring models used by Credit Karma, many banks, and increasingly by lenders, completely ignore paid collection accounts. This means if your lender or card issuer uses VantageScore, paying off your collections could give you a score improvement almost immediately after the status updates.

This is one reason why the score you see on a free monitoring app might look different from the score your mortgage lender pulls.

How Many Points Will My Credit Score Go Up?

This is one of the most searched questions about collections, and there’s no single answer. Here’s a realistic framework:

Factors that determine how much your score improves:

- Your starting score: If your score is already low, there’s more room to recover. If it’s in the mid-600s with one collection, the jump might be smaller.

- Age of the collection: Older collections (3+ years) already have diminishing impact. Paying them off may produce less noticeable improvement than paying a recent one.

- Number of collections: If you have multiple collections and pay one, the other negatives will continue to suppress your score. Paying all of them has a compounding positive effect.

- The balance amount: Higher-balance collection accounts typically carry more weight.

- Which scoring model applies: As shown above, FICO 8 may show no improvement; FICO 9 could show significant gains.

- Everything else on your report: High credit utilization, recent late payments, or multiple hard inquiries can cancel out any gains from paying collections.

Realistic ranges:

- FICO 8: 0–30 points improvement (possibly none)

- FICO 9 / VantageScore 4.0: 20–80+ points improvement if collections are the primary negative factor

What Can Slow Down Your Credit Recovery

Even after paying collections, these factors will hold your score back:

- High credit utilization – If you’re using more than 30% of your available credit limits, this single factor outweighs most positive changes

- Recent late payments on other accounts

- Multiple hard inquiries from recent loan or credit card applications

- Other derogatory items still reporting (charge-offs, judgments, etc.)

- No new positive history being added – payment history is 35% of your FICO score, and you need new on-time payments to rebuild it

What Happens to Collections on Your Credit Report After You Pay?

The 7-Year Rule Explained

Regardless of whether you pay a collection, it stays on your credit report for 7 years from the original delinquency date, the date you first missed a payment on the original account. The 7-year clock starts with that first missed payment, not when the account was sold to collections, not when you pay it off.

This is why a 6-year-old collection that you pay today will only be on your report for one more year, making the decision to pay it more nuanced than it might seem.

It’s also worth understanding the relationship between charge-offs and collections – sometimes what looks like one derogatory entry is actually two separate accounts (the original charge-off and the collection), both reporting simultaneously.

Medical Debt: The 2025 Rule Change You Need to Know

If you have medical collections, there’s important news: The Consumer Financial Protection Bureau (CFPB) finalized a rule in 2025 removing medical debt from credit reports entirely. This means medical collection accounts – whether paid or unpaid – should no longer appear on your credit report under the new rule.

If you see medical debt still reporting, this could be a reporting error that you have the right to dispute. A professional credit specialist can help you identify and challenge these entries.

How to Remove a Collection Account, Even After Paying

Here’s something most people don’t realize: just because you’ve already paid a collection doesn’t mean you’ve lost your leverage to have it removed entirely.

The Pay for Delete Strategy

Pay for Delete vs. Paid in Full is a distinction worth understanding deeply. With Pay for Delete, you negotiate to have the collection account removed from your credit report entirely in exchange for payment, rather than simply updating the status to “paid.”

While this strategy works better with third-party collection agencies than original creditors, it can be a powerful tool when executed correctly. Important caveat: Get any agreement in writing before making any payment. Verbal agreements with collectors are difficult to enforce.

Writing a Goodwill Letter That Works

If you’ve already paid off the collection without a Pay for Delete agreement, you still have an option: the goodwill letter. This is a written request to the creditor or collection agency asking them to remove the negative entry as a gesture of goodwill.

Goodwill letters work best when:

- You had a strong payment history before the collection

- The collection resulted from a temporary hardship (job loss, medical emergency, etc.)

- The account is fully paid

This strategy typically works better with original creditors than third-party collectors, but it’s always worth attempting. At The Phenix Group, our credit specialists craft strategic goodwill letters as part of our attorney-engaged credit repair process – and we’ve helped clients get entries removed even after they’ve already paid.

Disputing Inaccurate or Unverifiable Collections

A 2024 Consumer Reports study found that 27% of people who reviewed their credit reports found errors that affected their score. Collection accounts are among the most error-prone entries.

You have the legal right under the Fair Credit Reporting Act (FCRA) to dispute any inaccurate, outdated, or unverifiable information on your credit report. If a collector cannot prove the debt is legitimately yours and accurately reported, it can be removed entirely.

For a full breakdown of the dispute process, see our guide to removing collections from your credit report.

What to Do Right Now to Speed Up Your Credit Recovery

Paying off a collection is one positive step, but it’s rarely enough on its own. Here’s a strategic action plan to rebuild your credit as efficiently as possible.

Step-by-Step Action Plan After Paying Collections

Step 1: Confirm the update is reporting correctly

Pull your credit reports from all three bureaus (Equifax, Experian, TransUnion) 60 days after your payment and verify the account shows “paid in full” or “paid collection.” Look for any discrepancies between bureaus.

Step 2: Check for errors and dispute anything inaccurate

Look for wrong balances, incorrect delinquency dates, or duplicate entries. If you find any, file formal disputes with the respective bureaus. Understanding what is a good credit score and where yours currently sits is a critical benchmark.

Step 3: Lower your credit utilization immediately

Credit utilization (the amount you owe vs. your credit limits) accounts for 30% of your FICO score and updates every billing cycle. Getting your utilization below 30% – ideally below 10% – can produce a noticeable score bump within 30 days, no dispute required.

Step 4: Add positive payment history

Since payment history is 35% of your FICO score, the fastest way to rebuild is to add consistent, on-time payments. A secured credit card or credit-builder loan can start adding positive history within one billing cycle.

Step 5: Avoid new hard inquiries

Each new credit application triggers a hard inquiry that can drop your score by 5–10 points. While you’re rebuilding, be strategic about applying for new credit.

Step 6: Consider professional credit repair for complex situations

If you have multiple collections, charge-offs, or a mortgage deadline approaching, DIY efforts often fall short. Understanding DIY credit repair vs. professional help can save you months of frustration and costly mistakes.

Should You Pay Old Collections? A Strategic Guide

This is a nuanced question, and the right answer depends entirely on your specific situation.

When Paying Collections Helps

You’re applying for a mortgage soon

Most credit repair services for home buyers know that many mortgage lenders require all open collections to be paid or settled before approval. Even if it doesn’t boost your score, it removes a lender objection.

The collection is recent (less than 2 years old)

Newer collections carry more weight, and paying them can produce more meaningful score improvement.

Your lender uses FICO 9 or VantageScore 4.0

Under these models, paid collections are completely ignored. The ROI is much higher.

You can negotiate a Pay for Delete

If you can get the entry removed entirely, paying almost always makes sense regardless of timing.

When Paying Could Backfire

The collection is very old (5–6 years)

Paying an old collection can sometimes “re-age” the account if not handled correctly, briefly extending the negative impact. Always consult a professional before paying old debts.

The debt has passed the statute of limitations

Paying can reset the statute of limitations in some states, reopening your legal exposure. Verify your state’s rules first.

You can’t negotiate favorable terms

If you’re simply going to pay full balance with no agreement to update or remove the account, there may be better uses for that money.

For personalized guidance on your specific accounts, our specialists offer a free credit analysis that evaluates the optimal strategy for your credit goals and timeline. We’ve helped clients across our credit repair service areas navigate these exact decisions.

Working With a Professional Credit Repair Company

Navigating collections, FICO versions, Pay for Delete negotiations, and dispute processes simultaneously is genuinely complex, and mistakes can cost you months of progress.

At The Phenix Group, our Fort Worth credit repair specialists and nationwide team use an attorney-engaged process that goes beyond simple bureau disputes. We work directly with collection agencies, original creditors, and bureaus simultaneously, holding all parties accountable to FCRA and FDCPA requirements.

Most of our clients see results within 60 days of starting the program. Review our credit repair cost and pricing to understand how the program works, or start with a no-cost, no-obligation credit analysis.

Frequently Asked Questions

How long after paying off collections does my credit score improve?

The collection account status typically updates on your credit report within 30–60 days after payment. Credit score improvement varies by scoring model, FICO 9 and VantageScore 4.0 may show improvement quickly once the account is marked paid, while FICO 8 (the most widely used model) may show little to no score change. Meaningful overall credit recovery typically takes 3–12 months.

Does paying collections remove it from my credit report?

No. Paying a collection account changes its status to “paid” but does not automatically remove it. The account will remain on your credit report for 7 years from the original delinquency date. To have it removed, you need to either negotiate a Pay for Delete agreement, submit a successful goodwill letter, or dispute inaccurate information.

Will paying off collections help me get approved for a mortgage?

Yes, in most cases. Most mortgage lenders require that open collection accounts be paid or settled before approval. Even if paying doesn’t significantly raise your score, it removes a major lender objection and improves your chances of approval.

How many points will my credit score go up after paying collections?

This depends on your overall credit profile, the scoring model used, and the age and balance of the collection. Under FICO 8, the increase may be 0–30 points. Under FICO 9 or VantageScore 4.0, the increase could be 20–80+ points if collections were your primary negative factor.

Should I pay old collections that are about to fall off my report?

A: Generally, no, if the collection is within 6–12 months of its 7-year removal date, paying it produces minimal score benefit and may complicate the situation. However, if a mortgage lender requires it or you can negotiate removal, paying may still be appropriate. Consult a credit specialist before acting.

What is Pay for Delete and does it work?

Pay for Delete is a negotiation strategy where you offer to pay the collection in exchange for the agency removing the account from your credit report entirely. It’s more likely to work with third-party collection agencies than original creditors, and all agreements must be in writing. See our full guide to Pay for Delete vs. Paid in Full.

How quickly can The Phenix Group help improve my credit?

Most clients begin seeing score movement within 60 days of starting the program. The full program typically takes 6–12 months depending on the complexity of your credit file. We offer a free credit analysis to assess your specific situation and provide a realistic timeline.