Finding National Credit Systems on your credit report can feel like the floor dropped out beneath you. Your credit score takes a sudden hit, the phone starts ringing with collection calls, and you’re left wondering, do I owe this? Is this legitimate? And most importantly, what can I do about it?

Take a breath. You have more power than you think.

In this guide, we break down exactly who National Credit Systems (NCS) is, why they appear on your credit report, how their collections affect your score, and most critically, the five proven steps you can take to fight back, protect your rights, and potentially remove them from your credit report entirely.

Whether you’ve received a collection notice in the mail, spotted the listing on your report, or gotten a surprise phone call, this guide covers everything you need to know about National Credit Systems collections.

What Is National Credit Systems?

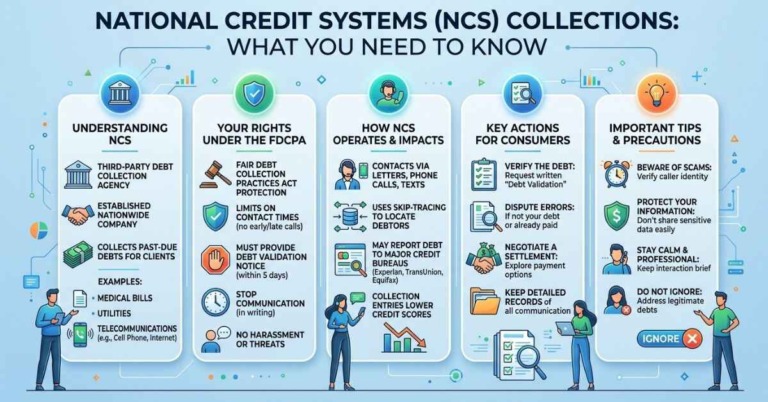

National Credit Systems, Inc. (NCS) is a third-party debt collection agency headquartered in Atlanta, Georgia. Founded in 1991, it primarily specializes in collecting unpaid debts for the multifamily residential industry, which is a formal way of saying: landlords and apartment management companies.

If you’ve left an apartment with an unpaid balance, whether it’s back rent, property damage charges, or early termination fees, there’s a good chance the property management company sent that debt to NCS for collection.

NCS Contact Information:

- Address: 3750 Naturally Fresh Blvd, Atlanta, GA 30349 / P.O. Box 312125, Atlanta, GA 31131

- Website: nationalcreditsystems.com

NCS is a legitimate, licensed collection agency authorized to collect debt across the United States. That doesn’t mean, however, that everything they report is accurate, or that you should simply accept the listing without reviewing it carefully.

Why Is National Credit Systems on My Credit Report?

When NCS appears on your credit report, one of two things typically happened:

- They purchased your debt from your former landlord or property management company (usually for pennies on the dollar after a charge-off).

- They were hired to collect the debt on behalf of your landlord without purchasing it outright.

Either way, their appearance on your report signals that a past rental-related account has gone seriously delinquent. Common reasons include unpaid rent, unit damage beyond normal wear and tear, lease break fees, and unpaid utility accounts tied to the rental.

It’s also worth noting that errors are common as debt transfers between creditors and collectors. The Public Interest Research Group (PIRG) has found that roughly 79% of credit reports contain some type of error, meaning your NCS listing may be inaccurate, duplicated, or not even yours.

How National Credit Systems Collections Damage Your Credit Score

A collection account from NCS acts as a negative mark on your credit report and can drag your score down significantly, sometimes by 50 to 100+ points, depending on your overall credit history. Worse, a collection account can remain on your credit report for up to seven years from the date of first delinquency.

During that time, it can affect your ability to:

- Qualify for a mortgage or home loan

- Secure an auto loan or credit card

- Rent a new apartment (many landlords pull credit)

- Pass certain employer background checks

Here’s something many people don’t realize: simply paying the NCS balance does not automatically remove the collection from your credit report. It changes the status from “unpaid” to “paid”, but the account stays on your report for the full seven years and can still drag your score. This is why how you handle NCS matters so much.

5 Proven Steps to Remove National Credit Systems From Your Credit Report

Step 1: Request Debt Validation Immediately

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to demand that NCS prove the debt is legitimately yours before you pay a single dollar. Send a debt validation letter via certified mail with return receipt within 30 days of their first contact. Your letter should request:

- The name and address of the original creditor

- A complete breakdown of the amount owed

- Evidence that NCS is licensed to collect in your state

- Proof that they have the legal right to collect the debt

Once NCS receives your validation request, they are legally required to stop all collection activity until they provide proof. If they cannot validate the debt, they must stop reporting it to the credit bureaus, and it must be removed from your report. This step alone resolves a significant number of collections accounts.

Step 2: Review for Errors and Dispute With Credit Bureaus

Pull your credit reports from all three bureaus, Equifax, Experian, and TransUnion, at AnnualCreditReport.com. Compare the NCS listing carefully against your own records. Look for:

- Incorrect balance amounts

- Wrong original creditor name

- Inaccurate dates (especially the original delinquency date)

- Duplicate entries for the same account

- Accounts that don’t belong to you at all

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any inaccurate or incomplete information. File disputes directly with each bureau that is reporting the error. The bureau must investigate within 30 days, and if NCS cannot verify the accuracy of the information, it must be corrected or removed.

Step 3: Negotiate a Pay-for-Delete Agreement

If the debt is valid and within the statute of limitations, a pay-for-delete agreement may be your best strategy. This is an arrangement where you agree to pay NCS, often for less than the full balance, in exchange for their agreement to completely remove the collection entry from your credit report.

Important details about pay-for-delete with NCS:

- NCS does not always agree to pay-for-delete, it’s not guaranteed

- Always get the agreement in writing before making any payment

- Start negotiations below the full balance, NCS likely purchased the debt at a significant discount

- Confirm the specific action: “delete” (not just “update to paid”) is what you want in writing

For a deeper comparison of your options, see our guide on pay for delete vs paid in full which explains exactly how each strategy affects your credit score differently.

“I am writing to offer resolution of Account [#], originally held by [Creditor Name]. In exchange for payment of $[Amount], I request that National Credit Systems, Inc. agree to delete all reporting related to this account from Equifax, Experian, and TransUnion within 30 days of payment clearing. Please confirm this agreement in writing before payment is remitted.”

Step 4: Send a Cease and Desist Letter (If Needed)

If NCS is harassing you with repeated calls, contacting you at your workplace, or using abusive language, you have the right to demand they stop all direct contact. A cease and desist letter, again sent via certified mail, legally forces them to stop calling and writing.

Understand what a cease and desist does and does not do: it stops the phone calls and letters, but it does not eliminate the debt. NCS can still take legal action to collect. However, it does give you breathing room to strategize, and any violation of your cease and desist request may constitute a FDCPA violation you can act on.

Step 5: Work With a Credit Repair Specialist

Dealing with NCS can be complex, time-consuming, and stressful, especially if you’re preparing for a major financial milestone like buying a home. If you’re facing an NCS collection and aren’t sure of the best path forward, working with a professional credit repair company like The Phenix Group gives you a significant advantage.

Unlike generic credit repair companies that only send online bureau disputes, The Phenix Group’s attorney-enforced audit process investigates at the bureau level and directly engages the original creditor and collection agency, holding them accountable to federal and state consumer protection laws.

We offer a free credit report analysis and consultation so you know exactly where you stand before you pay anyone anything.

Should You Pay National Credit Systems? (The Answer Might Surprise You)

Many people assume paying NCS immediately will clean up their credit. The reality is more nuanced. Here’s a quick breakdown:

| Action | Credit Report Impact | When It Makes Sense |

|---|---|---|

| Pay in full (no agreement) | Account stays 7 years, updates to “Paid Collection” | Only if required by a lender before closing |

| Pay for delete | Account removed entirely if NCS agrees | Valid debt within statute of limitations |

| Dispute (errors found) | Account removed if not verified | Inaccurate, incomplete, or unverifiable info |

| Wait out statute of limitations | Account falls off after 7 years automatically | Old debt near expiration; you cannot be sued |

| Do nothing | Account stays + risk of lawsuit/judgment | Not recommended |

Always check the date of first delinquency before making any payment or acknowledgment. Depending on your state, once the statute of limitations expires for collection lawsuits, you cannot be taken to court, though the debt can still appear on your report.

What to Do If National Credit Systems Sues You

While lawsuits are not the norm, NCS and other collection agencies do file them, particularly for larger balances. If you are served with a lawsuit from National Credit Systems, do not ignore it. Ignoring a debt collection lawsuit results in a default judgment against you, which can lead to:

- Wage garnishment

- Bank account levies

- Liens placed against your property

- A court judgment on your credit report

You typically have 14 to 30 days to file a written response (Answer) with the court, depending on your state. In your response, you can raise defenses such as the statute of limitations, lack of proper debt validation, or that the amount claimed is inaccurate.

The Phenix Group can connect you with an attorney who can review your case and file a response on your behalf. Don’t wait, contact us for a free consultation the moment you’re served.

Your Rights Under the FDCPA and FCRA

Two federal laws protect you in every interaction with National Credit Systems:

The Fair Debt Collection Practices Act (FDCPA) prohibits NCS from:

- Calling before 8 AM or after 9 PM in your local time zone

- Using threatening, obscene, or abusive language

- Falsely claiming to be attorneys, law enforcement, or government agents

- Threatening arrest or imprisonment for unpaid debt (illegal)

- Contacting you after receiving a proper cease and desist request

- Reporting inaccurate information to credit bureaus

The Fair Credit Reporting Act (FCRA) gives you the right to:

- Dispute inaccurate or incomplete information on your credit report

- Have unverified information removed within 30 days

- Sue credit bureaus and collection agencies for willful violations

If NCS violates either of these laws, you may be entitled to statutory damages. Document every interaction, save letters, note call times, and keep copies of all correspondence.

NCS Complaints: BBB and CFPB Records You Should Know About

National Credit Systems has a history of consumer complaints filed with both the Better Business Bureau (BBB) and the Consumer Financial Protection Bureau (CFPB). Complaints commonly allege harassment, inaccurate debt amounts, failure to validate debts, and errors in credit bureau reporting.

In 2017, NCS was the subject of a lawsuit for sending collection letters that a court found to be “false, misleading and confusing to the unsophisticated consumer”, a direct violation of the FDCPA. The debt involved was also time-barred, meaning the statute of limitations had already expired.

You can file a complaint with the CFPB at consumerfinance.gov/complaint or with the FTC at reportfraud.ftc.gov if you believe NCS has violated your rights.

Rebuilding Your Credit After NCS Is Removed

Getting NCS off your report is a win, but it’s just the start. Whether your goal is to qualify for a mortgage, finance a vehicle, or simply restore your financial standing, the next step is actively rebuilding your credit profile. Key strategies include:

- Ensuring all current accounts are paid on time, payment history is 35% of your score

- Reducing credit card utilization below 30%

- Avoiding new collection accounts and charge-offs

- Monitoring your report regularly for new errors

- Working with a credit specialist to address any remaining negative items

The Phenix Group specializes in getting clients mortgage-ready, even when they start from a challenging credit position. Our team works directly with lenders and underwriters, not just the credit bureaus, to get you cleared to close. Learn more about our home ownership credit repair services.