If you’ve ever Googled “how much does credit repair cost,” you already know the answers online range from vague to downright misleading. So let’s cut straight to the facts.

Professional credit repair typically costs $50 to $150 per month, plus a one-time setup fee ranging from $15 to $200. Over a typical program of three to six months, most people spend between $300 and $1,000 total. But that number varies significantly based on who you hire, what your credit file looks like, and which pricing model the company uses.

At The Phenix Group, we believe in full transparency before you spend a single dollar. That’s why we start every client relationship with a free credit analysis, so you know exactly what you’re dealing with and what it will realistically take to fix it. No surprise fees. No pressure. Just a clear plan.

In this guide, we’ll break down every type of credit repair fee, compare the true cost of doing it yourself versus hiring a professional, and show you how to make sure every dollar you spend goes toward real, lasting results.

Credit Repair Pricing at a Glance: What to Expect

Before we go deep on each pricing model, here’s a clear snapshot of what professional credit repair costs across the board:

| Fee Type | Typical Range | Notes |

|---|---|---|

| Setup / First Work Fee | $15 – $200 | Covers initial credit pull and case setup. Many companies charge this as equal to the monthly fee. |

| Monthly Subscription Fee | $50 – $150/month | Most common model. Ongoing disputes and monitoring included. |

| Pay-Per-Delete Fee | $25 – $150 per item | Charged only when a negative item is successfully removed. |

| Tiered/Premium Packages | $100 – $180+/month | Adds credit monitoring, identity theft protection, score tracking. |

| Total (3-month program) | $165 – $650 | Avg. setup + 3 months of service |

| Total (6-month program) | $315 – $1,100 | Avg. setup + 6 months of service |

Keep in mind: the cheapest option is rarely the most effective, and the most expensive isn’t always the best. What truly matters is what you get for that fee, and how many errors can realistically be removed from your report.

What Is Credit Repair and What Does It Actually Fix?

Credit repair is the process of identifying and challenging inaccurate, outdated, or unverifiable negative information on your credit reports. Your credit profile is maintained by the three major credit bureaus, Equifax, Experian, and TransUnion, and errors are far more common than most people realize.

According to Consumer Reports, more than 27% of people who reviewed their credit reports found errors serious enough to potentially affect their score. Common issues include:

- Payments incorrectly reported as late or missed

- Accounts that don’t belong to you (often linked to identity theft)

- Outdated collection accounts that should have been removed

- Incorrect account balances or credit limits

- Duplicate accounts or accounts listed multiple times

Under the Fair Credit Reporting Act (FCRA), you have the legal right to dispute any information on your credit report that you believe to be inaccurate. Credit repair companies, including The Phenix Group’s attorney-backed credit repair process, use this right strategically on your behalf, with proper documentation and legal oversight to ensure disputes are handled correctly and permanently.

Credit Repair Pricing Models: How Companies Charge

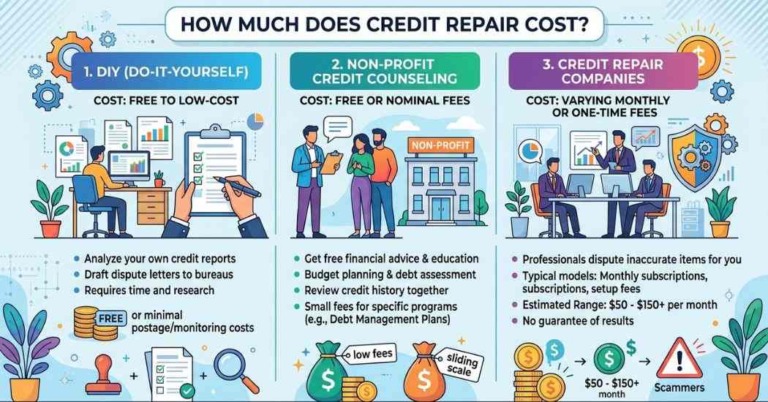

Understanding how a company charges you is just as important as understanding how much. There are three primary pricing models used in the credit repair industry today. Knowing which one a company uses, before you sign anything, can save you hundreds of dollars.

Monthly Subscription Model

This is the most common pricing structure. You pay a recurring monthly fee, typically $50 to $150 per month, in exchange for ongoing dispute management, bureau communications, and progress tracking. Most subscription-based companies also charge a one-time setup fee (often equal to one month’s payment) at the start of your program.

The advantage is predictable billing. The risk is that some companies have little incentive to resolve your issues quickly, more months enrolled means more revenue for them. At The Phenix Group, our pricing is built around active work, not prolonged enrollment. Our goal is to get you results in the shortest possible time, not the longest.

Pay-Per-Delete Model

Some companies charge you only when a negative item is successfully removed from your report, typically $25 to $150 per deletion, depending on the type and severity of the item. On the surface, this sounds appealing. In practice, it can lead to much higher total costs if you have multiple negative items, and it creates a perverse incentive to dispute only the easiest-to-remove items rather than the ones doing the most damage.

Tiered / Package Plans

Many larger credit repair companies offer tiered service packages ranging from $79 to $180+ per month. Lower tiers typically cover basic bureau disputes, while higher tiers add creditor intervention letters, identity theft monitoring, credit score tracking, and dedicated case management. For complex credit profiles, a higher-tier plan may genuinely accelerate results, but always ask specifically what each tier includes before committing.

What Does Your Credit Repair Fee Actually Cover?

One of the most common complaints about the credit repair industry is that consumers don’t know what they’re paying for month to month. Here’s what a legitimate, professional credit repair fee should cover:

- Credit report analysis: A thorough review of all three bureau reports to identify inaccurate, outdated, or unverifiable items

- Custom dispute letters: Professionally drafted letters to each bureau (not recycled generic templates)

- Creditor interventions: Direct contact with original creditors and collection agencies

- Compliance oversight: Ensuring all disputes comply with FCRA, FDCPA, and CROA requirements

- Progress tracking: Regular updates on dispute statuses across all three bureaus

- Credit education: Guidance on building and maintaining good credit going forward

At The Phenix Group, our real client results reflect what happens when all of the above is done correctly, with attorney engagement backing every step of the process. One of our clients went from a damaged credit profile to closing on their home in just three months, with a 150-point increase in their score.

DIY Credit Repair vs. Hiring a Professional: Cost Comparison

You have the right to dispute errors on your credit report yourself, for free. So why do people hire credit repair companies? Here’s an honest comparison so you can make the right decision for your situation.

| Factor | DIY Credit Repair | Professional Credit Repair |

|---|---|---|

| Cost | Free to low-cost (postage, certified mail) | $50–$150/month + setup fee |

| Time investment | 20–40+ hours over several months | Minimal, handled by your specialist |

| Legal knowledge required | High, FCRA, FDCPA, CROA | None, professionals handle compliance |

| Documentation management | You manage all paperwork and deadlines | Handled by your team |

| Dispute effectiveness | Can work for simple, clear errors | Much more effective for complex files |

| Attorney backing | None | Available with attorney-engaged companies |

| Risk of errors | High, missed deadlines, improper documentation | Low, professionals follow compliance protocols |

Bottom line: If you have one or two simple, obvious errors, DIY may work. But if your credit file has multiple negative accounts, collection disputes, identity theft markers, or you’re trying to qualify for a mortgage on a timeline, professional help is almost always worth the investment. You can learn more about this decision in our detailed breakdown of whether credit repair companies are worth it.

Is Credit Repair Worth the Cost? The ROI Breakdown

Here’s a question worth asking: what does bad credit actually cost you? The answer might surprise you.

A borrower with poor credit (say, a 580 score) applying for a $300,000 mortgage could be paying an interest rate 1.5–2.5% higher than someone with excellent credit. Over a 30-year loan, that difference translates to $80,000 to $150,000 in extra interest. Compare that to $600–$1,000 in credit repair fees, and the math becomes clear.

Credit repair also has a direct impact on:

- Auto loan rates: A 100-point score improvement can cut your interest rate by 3–5%

- Credit card APRs: Better scores unlock lower rates and higher limits

- Insurance premiums: In most states, credit scores affect what you pay for auto and homeowner’s insurance

- Rental approvals: Many landlords require minimum credit scores

If homeownership is your goal, our credit repair for home buyers program is specifically designed to align with mortgage timelines and lender requirements, giving you the best possible shot at qualifying with a rate that won’t haunt you for decades.

Why Attorney-Backed Credit Repair Is Different and Worth More

Not all credit repair is created equal. Most companies send the same recycled dispute letters that credit bureaus have seen thousands of times before, and often dismiss within days. The Phenix Group takes a fundamentally different approach: every dispute is backed by an independent law firm versed in consumer protection law.

This matters for three reasons:

- Legal leverage: When disputes are filed through an attorney-engaged process, creditors and bureaus take them more seriously. Non-compliance exposes them to legal liability, which gives your disputes real teeth.

- Accountability: Attorneys are bound by professional and ethical standards that general credit repair companies are not. That means higher accuracy, proper documentation, and compliance with the FCRA and FDCPA at every step.

- Lasting results: Disputes filed correctly don’t bounce back. Many consumers who attempt DIY repair or use low-quality services see negative items “reinsertion” – they come back. Attorney-engaged disputes are harder to reinsert because the original challenge was properly documented and legally grounded.

For a deeper look at how much a credit repair lawyer costs compared to our attorney-backed program, we’ve broken that down in detail as well.

What’s Included FREE with The Phenix Group

Many credit repair companies charge extra for services we provide at no additional cost. Here’s what comes free with every Phenix Group program:

- Free credit analysis: A full review of your Equifax, Experian, and TransUnion reports before you commit to anything

- Free consultation: A one-on-one session with a credit analyst to map out your situation and goals

- Free client setup: Our setup process typically takes 1–3 hours. Many companies charge hundreds of dollars for this, we don’t.

- Free credit report access: We pull your reports so you don’t have to navigate the confusing world of third-party services

- Free credit education: Understanding how credit works is essential to keeping your score strong long-term. We teach you, not just fix you.

Our average credit repair cost guide goes into further detail about what a typical client’s program looks like from start to finish.

Credit Repair Scams: Red Flags That Should Make You Run

The credit repair industry attracts its share of bad actors. Knowing how to spot a scam can save you not just money, but significant time and further damage to your credit. Here are the biggest red flags:

- They demand payment upfront – before any work is performed. Under the Credit Repair Organizations Act (CROA), credit repair companies cannot legally collect payment before services are rendered. Anyone asking for full payment upfront is likely breaking the law.

- They promise to remove ALL negative information – including accurate, verifiable items. Only inaccurate, outdated, or unverifiable information can legally be challenged. Anyone promising to wipe your entire credit history clean is either lying or planning something illegal.

- They tell you to avoid contacting the credit bureaus yourself, a major red flag. Contacting Equifax, Experian, and TransUnion is a fundamental part of the dispute process. Any company that discourages this is likely hiding something.

- They suggest creating a “new credit identity” (using a CPN or EIN instead of your SSN), this is illegal and can result in federal fraud charges.

- They won’t explain your legal rights legitimate companies are required to provide you with a written disclosure of your rights before signing any contract.

- They have no physical address or verifiable business history, always verify a company’s credentials, BBB rating, and track record before handing over any personal information.

Your Rights Under the Credit Repair Organizations Act (CROA)

The Credit Repair Organizations Act (CROA) is the primary federal law that governs credit repair companies. Understanding your rights puts you in control of the relationship, and protects you from bad actors. Under CROA, every legitimate credit repair company must:

- Provide you with a copy of “Consumer Credit File Rights Under State and Federal Law” before signing any contract

- Give you a written contract outlining the services to be performed, the timeframe, and the total cost

- Give you three business days to cancel without any penalty

- Not collect any fees until promised services have been fully delivered

- Not make false statements or guarantees about improving your credit

When you work with a company like The Phenix Group, where every dispute is attorney-engaged, these rights aren’t just legal obligations. They’re built into the way we operate.

How Long Does Credit Repair Take (and What Does It Cost Over Time)?

Credit repair is not an overnight process, and anyone who tells you otherwise is not being honest with you. Here’s a realistic timeline and associated cost range:

| Timeline | Typical Scenario | Estimated Cost |

|---|---|---|

| 30–60 days | 1–3 simple errors (wrong address, small outdated account) | $65–$350 total |

| 3–4 months | Multiple negative accounts, collections, late payments | $200–$750 total |

| 4–6 months | Complex files: judgments, multiple collection accounts | $350–$1,100 total |

| 6–12 months | Identity theft, bankruptcy-related disputes, multiple bureaus | $500–$1,500+ total |

Credit bureaus are legally required to investigate disputes and respond within 30 days. If the creditor cannot verify the information, it must be corrected or deleted. This 30-day cycle determines how fast your program can move, which is why working with an experienced team that files disputes correctly the first time matters so much.

Whether you’re in Houston, Chicago, El Paso, Pittsburgh, or anywhere across the country, The Phenix Group serves clients nationwide with the same attorney-backed, personalized approach. Our Fort Worth, TX headquarters is home to a team with over 80 years of combined credit industry experience.

Frequently Asked Questions About Credit Repair Costs

Most professional credit repair companies charge between $50 and $150 per month. The exact amount depends on the company, the pricing model they use, and the level of service included. Some higher-tier packages can reach $180+ per month but include credit monitoring and identity theft protection.

Yes, most companies charge a one-time setup or first work fee. This typically ranges from $15 to $200 and covers the cost of pulling your credit reports and setting up your case file. Some companies, including The Phenix Group, do not charge for basic client setup.

Yes. You can dispute errors on your own by contacting the three credit bureaus directly. This is free, though it requires significant time, documentation, and knowledge of consumer protection laws. For simple errors, DIY may be effective. For complex files, professional help typically delivers faster, more reliable results.

Credit bureaus must respond to disputes within 30 days. Simple cases may be resolved in 30–60 days. More complex files with multiple negative accounts typically take 3–6 months. Severe cases involving identity theft or bankruptcy may take 6–12 months or more.

In a pay-per-delete model, you only pay when a negative item is successfully removed from your credit report. Fees per deletion typically range from $25 to $150. While this sounds appealing, it can get expensive if you have many items to remove, and some companies may cherry-pick easier deletions rather than addressing the most damaging items first.

A legitimate credit repair company will give you a written contract, explain your right to cancel within three business days, not charge you before services are performed, and not promise to remove accurate information from your report. Look for verifiable business history, BBB accreditation, and real client testimonials. Avoid any company that suggests creating a “new credit identity.”

Not necessarily. Attorney-backed credit repair involves a law firm overseeing or directly handling disputes, which adds legal accountability to the process. At The Phenix Group, our attorney-engaged process does not require you to pay separate legal fees. The attorney oversight is built into our program as part of our commitment to compliance and effectiveness.

Credit repair focuses specifically on disputing and removing inaccurate or unverifiable negative items from your credit reports. Credit counseling is broader, it includes budgeting advice, debt management plans, and financial education. Some credit repair companies (like The Phenix Group) incorporate education into their programs, giving you both dispute resolution and the knowledge to protect your score long-term.

The Bottom Line: Credit Repair Is an Investment, Not Just an Expense

When you understand that a single percentage point improvement in your mortgage rate can save you tens of thousands of dollars over the life of a loan, the cost of credit repair starts to look very different. The question isn’t whether you can afford professional credit repair. For most people, the real question is whether you can afford not to pursue it.

At The Phenix Group, we never ask you to guess. Our process starts with a free, no-obligation credit analysis, a real look at your reports, conducted by an experienced analyst, with a transparent plan before you commit to anything. No cookie-cutter programs. No upfront payment pressure. Just honest guidance from a team with over 80 years of combined credit industry experience.

To see what’s possible, check out our real client results, including clients who gained 100+ points and closed on their first home within three months of starting their program.

Ready to find out what credit repair will cost for your specific situation? Schedule your free credit analysis today. It costs nothing, and it could change everything.