If Southwest Credit Systems collectors have contacted you by phone, email, or letter, or if you just spotted ‘SW Crdt Sys’ on your credit report, you are in the right place. This guide tells you exactly who they are, which companies they collect for, what they can and cannot legally do, and what steps to take right now to protect your credit score.

Southwest Credit Systems, also operating under the name SWC Group, is a legitimate third-party debt collection agency headquartered in Carrollton, Texas. They have been in business since 1974 and have held BBB accreditation since 1976. However, ‘legitimate’ does not mean ‘error-free’, and it certainly does not mean you should pay without asking questions first.

What Is Southwest Credit Systems (SWC Group)?

Southwest Credit Systems LP is a third-party debt collection agency, meaning they do not own the debts they collect. Instead, they are hired by original creditors to pursue past-due balances on their behalf. The original creditor retains ownership of the debt, which is important to understand when it comes time to negotiate.

The company manages billions of dollars in receivable accounts across multiple industries. When you see SWC Group on your caller ID or SW Crdt Sys on your Experian, Equifax, or TransUnion credit report, it is because one of their clients has hired them to contact you about an outstanding balance.

Despite their long history, Southwest Credit Systems collectors have generated over 1,095 complaints filed with the Consumer Financial Protection Bureau (CFPB). Common complaints include failure to provide written debt notification, attempts to collect debts consumers say are not theirs, and improper credit reporting.

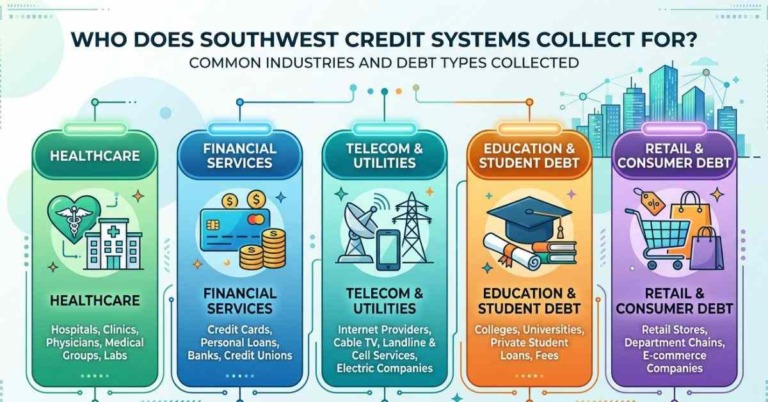

Who Does Southwest Credit Systems Collect For? (Industry Breakdown)

This is the question most people are asking when they search for Southwest Credit Systems collectors. Here is a complete breakdown of the industries and types of clients that hire SWC Group:

Telecommunications

This is SWC Group’s biggest collection sector. They collect past-due balances for major telecom providers including T-Mobile (confirmed via BBB complaint responses from SWC directly), Comcast, and other cable and internet providers. If you canceled a contract early, missed final payments, or had a service dispute, your account may have been sent to Southwest Credit Systems.

Toll Road Authorities

SWC Group is the contracted collection agency for the Central Texas Regional Mobility Authority, one of Texas’s largest toll road operators. If you drove through a toll and did not pay, Southwest Credit Systems collectors may be contacting you on their behalf. This is one of the most common sources of surprise collection notices in Texas.

Utility Companies

Unpaid gas, electricity, and water bills are commonly placed with SWC. If you moved and left a balance with a utility provider, or had a disputed bill that went unresolved, it could have been forwarded to Southwest Credit Systems for collection.

Healthcare Providers

Medical debt is among the fastest-growing categories for collection agencies. Southwest Credit Systems collects for medical service companies, including hospital bills, emergency services, and physician invoices. This is particularly significant because medical debt rules under credit reporting have recently changed, making disputes in this category especially viable.

Property Management

Landlords and property management companies hire SWC Group to recover unpaid rent, lease-break fees, and damage costs. If you vacated a rental unit with an outstanding balance, you may encounter Southwest Credit Systems collectors.

Financial Institutions

SWC also manages collections for certain financial institutions and credit providers. This can include unpaid credit card balances, personal loans, or bank fees that have reached delinquency.

How Southwest Credit Systems Affects Your Credit Score

A collection entry from Southwest Credit Systems collectors is not a minor inconvenience. Here is what you should expect:

• A new collection account can lower your credit score by 50 to 100 points or more, depending on the rest of your credit profile.

• The collection remains on your report for up to seven years from the date of original delinquency, even if you pay it.

• Mortgage lenders, auto lenders, and landlords frequently deny applications based on active collection accounts.

• Even paid collections can result in higher interest rates on approved loans.

• In states where insurers use credit scoring, a collection can also raise your insurance premiums.

This is why it matters whether the debt is accurate, valid, and reportable, not just whether you technically owe it.

What to Do If Southwest Credit Systems Contacts You (Step-by-Step)

Do not panic, and do not pay immediately. Here is the correct sequence of steps:

- Stay calm and document the contact. Write down the date, time, phone number, what was said, and the name of the representative. Save any voicemails.

- Request a written debt validation notice. Under the FDCPA, Southwest Credit Systems is required to send you a written notice within 5 days of first contact. If they have not, demand one immediately in writing.

- Dispute within 30 days. If you believe the debt is inaccurate, not yours, already paid, or past the statute of limitations, send a written dispute by certified mail within 30 days of their first contact. SWC must stop collection activity until they verify the debt.

- Check your credit report. Pull your reports from Experian, Equifax, and TransUnion at AnnualCreditReport.com. Look for the entry labeled ‘SW Crdt Sys’ and compare the amount, date of original delinquency, and creditor name against your records.

- Dispute inaccuracies with the credit bureaus. If the entry contains errors, wrong amount, wrong date, not your account, file a formal dispute with each bureau that shows the error. Bureaus have 30 days to investigate.

- Consider professional help. If the debt is disputed, the entry is harming your ability to qualify for a mortgage or loan, or you are unsure of your next step, working with a credit repair specialist who understands the dispute process can save you significant time and protect your rights. You can explore credit repair services to better understand your options.

Your FDCPA Rights When Dealing with SWC Group Collectors

The Fair Debt Collection Practices Act (FDCPA) is a federal law that governs every move Southwest Credit Systems collectors are allowed to make. Knowing these rights puts you in control of the situation:

• SWC cannot call you before 8 a.m. or after 9 p.m. in your local time zone.

• They cannot call your workplace if you tell them your employer disapproves of such calls.

• They cannot use abusive, threatening, or profane language.

• They cannot threaten legal action they do not intend to take, or misrepresent the amount you owe.

• They must provide written verification of the debt if you request it within 30 days.

• They must stop all collection calls if you send a written cease-and-desist letter by certified mail (though they can still take legal action if warranted).

Understanding these rights is critical. If you want to learn more about how disputes and protections work together, review how credit repair works.

Each FDCPA violation can entitle you to up to $1,000 in statutory damages plus attorney fees. If Southwest Credit Systems collectors have harassed you, made threats, or reported inaccurate information, document every instance.

How to Remove Southwest Credit Systems from Your Credit Report

Removal is possible, but the strategy depends on your specific situation. Here are the legitimate paths:

Dispute Inaccurate or Unverifiable Debt

If the debt is not yours, contains errors, or SWC cannot verify it within 30 days of your dispute, the credit bureaus are required to remove it. This is the cleanest and most permanent removal method.

Pay-for-Delete Agreement

If the debt is valid, you may negotiate a pay-for-delete agreement with Southwest Credit Systems, they agree to remove the collection from your credit report in exchange for payment (full or settled). Importantly, SWC’s own policy states they submit deletions to the bureaus 60 days after an account is paid or settled, based on confirmed BBB complaint responses. Get any pay-for-delete agreement in writing before making payment.

Goodwill Deletion

If you have already paid the debt, you can write a goodwill letter requesting that SWC remove the entry as a gesture of goodwill. This is less reliable than a formal dispute, but it can work, particularly for consumers with an otherwise clean payment history.

If you want to better understand who is behind these accounts and how they operate, you can review a detailed breakdown of who Southwest Credit Systems is.

Statute of Limitations

Every state has a statute of limitations on how long a creditor can sue you to collect a debt. In Texas, this is generally 4 years. If the debt is beyond the SOL, collectors can still contact you and still report it, but they cannot successfully sue you. Do not make any payment or written acknowledgment on an old debt before confirming where it stands with the SOL in your state.

Can Southwest Credit Systems Sue You?

Yes, if you ignore Southwest Credit Systems collectors entirely and the debt is valid and within the statute of limitations, they have the legal right to file a lawsuit. If they obtain a court judgment against you, they may be able to garnish your wages or levy your bank account, subject to legal limits.

This is not a threat designed to scare you into paying, it is a reality that makes taking informed action more important than doing nothing. The right action is not always payment. It may be a dispute, a validation request, or a negotiated settlement. Do not make that decision without understanding your full picture.

Frequently Asked Questions

Q: Is Southwest Credit Systems a legitimate debt collector?

Yes. Southwest Credit Systems LP (SWC Group) is a real, licensed debt collection agency founded in 1974 and headquartered in Carrollton, Texas. They are accredited by the BBB and regulated under the FDCPA and FCRA. However, being legitimate does not mean every debt they report is accurate or that you have no options.

Q: What companies does Southwest Credit Systems collect for?

SWC Group collectors work on behalf of telecom companies (including T-Mobile), Comcast and other cable providers, the Central Texas Regional Mobility Authority (toll roads), utility companies, healthcare providers, property managers, and financial institutions.

Q: Why does ‘SW Crdt Sys’ appear on my credit report?

‘SW Crdt Sys’ is how Southwest Credit Systems or SWC Group appears on credit reports from Experian, Equifax, or TransUnion. It indicates that a collection account has been reported by this agency on behalf of an original creditor.

Q: Does Southwest Credit Systems buy debt, or do they collect on behalf of creditors?

SWC Group is not a debt buyer. They are a third-party collection agency, meaning the original creditor still owns the debt. Southwest Credit Systems is contracted to collect it on their behalf. This matters because your negotiation may ultimately involve the original creditor.

Q: How long can Southwest Credit Systems stay on my credit report?

A collection from Southwest Credit Systems can remain on your credit report for up to 7 years from the date of original delinquency, not the date SWC contacted you. Paying the debt does not automatically remove it, though you can negotiate a pay-for-delete agreement.

Q: Can I request Southwest Credit Systems stop calling me?

Yes. Under the FDCPA, you can send a written cease-and-desist letter by certified mail. Once received, SWC must stop calling you (they may only contact you to confirm receipt or notify you of legal action). This does not eliminate the debt.

Q: Can Southwest Credit Systems collectors sue me?

Yes, if the debt is within your state’s statute of limitations and remains unpaid. A successful judgment could result in wage garnishment or bank levies. This is why professional guidance on whether to dispute, settle, or pay is important before taking any action.

Q: What is a debt validation letter and should I request one?

A debt validation letter is a written notice from SWC that confirms the debt they are attempting to collect, including the amount, the original creditor, and proof that they have the right to collect. You have 30 days from first contact to request one. During this window, SWC must pause collection activity. If they cannot validate the debt, they must cease collection and request removal from your credit report.

Q: How does The Phenix Group help with Southwest Credit Systems?

The Phenix Group provides attorney-engaged credit repair and dispute services. We review your credit reports, identify whether the SWC entry is accurate and reportable, develop a custom dispute or negotiation strategy, and work directly with the bureaus, creditors, and collection agencies on your behalf.

For more real-world results and case outcomes, you can also explore success stories to see how similar cases have been handled.

Take Control of Your Credit, The Phenix Group Can Help

Dealing with Southwest Credit Systems collectors does not have to mean stress, confusion, or accepting an entry on your credit report without question. Whether the debt is valid, disputed, or the result of an error, you have legal rights, and you have options.

At The Phenix Group, we help consumers in Texas and across the country understand exactly where they stand, build a smart strategy, and take action to restore accuracy to their credit reports. Our approach goes beyond standard bureau disputes, we engage directly with creditors, collection agencies, and bureaus using the full weight of consumer protection law.