If someone has promised you a ‘credit sweep service’ that will wipe your credit report clean — you need to read this before you hand over a single dollar. Credit sweeps are one of the most misunderstood (and most abused) terms in the personal finance space, and the consequences of getting caught up in a fraudulent one can follow you for years.

At The Phenix Group, we hear from clients every week who were pitched a credit sweep as a quick fix. Our goal with this guide is simple: give you the complete, honest picture of what credit sweeps are, why they are typically illegal, what the law says about them, and what actually works to repair your credit legally and effectively.

Our attorney-backed credit repair services follow every rule in the book, and they deliver real, lasting results. But before we get into that, it’s critical you understand exactly what you may have been offered.

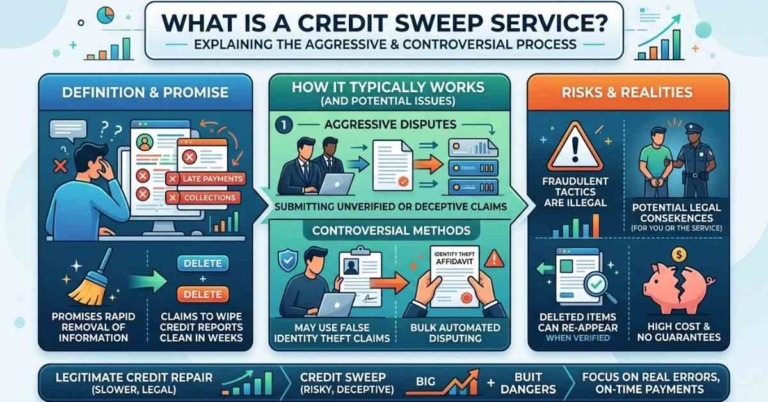

Understanding Credit Sweeps: Definition and How They Work

A credit sweep service, in the context of credit repair fraud, is a scheme in which a company or individual disputes every single item on your credit report, not just the inaccurate ones, often by falsely claiming that all of those accounts resulted from identity theft.

The appeal is obvious. If every negative mark on your report gets disputed and removed, you’d have a clean slate. The problem? That’s not how the law works, and in most cases, filing disputes for accounts that are actually yours is illegal.

We’ve covered the legal question in depth on our companion article: is a credit sweep legal? Here’s the short version: it’s not, unless every item on your report is genuinely fraudulent, which is virtually never the case.

The Step-by-Step Process of a Credit Sweep Scam

Here’s exactly how a fraudulent credit sweep service operates, so you know what to look for:

- A company contacts you (often unsolicited) promising to remove ALL negative items from your credit report, bankruptcies, foreclosures, collections, late payments, everything.

- They file a dispute for every single account on your report, typically claiming each one is the result of identity theft.

- To support these claims, some will falsify police reports in your name, a federal crime that you may not even be aware of until law enforcement comes knocking.

- Even in the ‘best case’ scenario where items are temporarily removed, they reappear the following month when creditors re-verify the accounts.

- You are left with a damaged credit history, potential criminal exposure, and a lighter wallet.

Why Credit Bureaus and Law Enforcement Take This Seriously

The three major credit reporting agencies, Equifax, Experian, and TransUnion, have seen enough credit sweep attempts that they’ve developed sophisticated systems to flag mass disputes. When every account on a report is disputed at once, it triggers fraud detection protocols.

More importantly, law enforcement agencies have actively prosecuted companies engaged in credit sweep fraud. In 2013, a Las Vegas company called Tradeline Pros was investigated by the Metropolitan Police Department and the U.S. Secret Service after filing over 174 fraudulent police reports to support mass credit disputes. The defendants faced charges including racketeering and forgery. This is not a hypothetical risk, it’s a documented reality.

Is a Credit Sweep Legal? What the Law Actually Says

The Fair Credit Reporting Act (FCRA)

The FCRA governs how credit bureaus must respond to disputes. It does allow for the removal of items tied to proven identity theft, but it requires a legitimate police report, an identity theft affidavit, and documentation. Filing a false identity theft claim to trigger disputes is a violation of federal law. The FCRA is not a loophole, it’s a protection that only works when the underlying claim is genuine.

The Credit Repair Organizations Act (CROA)

The CROA sets strict rules for any company offering credit repair services. Under this law, credit repair companies cannot:

- Charge fees before delivering services

- Make false or misleading claims about your credit history

- Advise you to make misrepresentations to credit bureaus

- Create a ‘new identity’ profile or use fraudulent means to alter your report

Any company offering a credit sweep is almost certainly violating the CROA. For more on what legitimate credit repair can and cannot do, read our full breakdown of facts about credit repair.

The Telemarketing Sales Rule (TSR)

The FTC’s Telemarketing Sales Rule also applies to credit repair companies that market their services via phone or online. It prohibits advance fees, deceptive claims, and unfair practices. Companies violating the TSR face civil penalties and enforcement actions from the FTC.

7 Red Flags That a ‘Credit Sweep Service’ Is a Scam

Before you sign anything or share your personal information, watch for these warning signs:

- They promise to remove ALL negative items, regardless of whether they are accurate or not

- They require upfront payment before providing any service, this alone is a CROA violation

- They ask you to sign blank paperwork or forms with missing information

- They guarantee results in 24–72 hours or claim to create a ‘new credit identity’ for you

- They suggest filing a police report claiming identity theft, even if you don’t believe your identity was stolen

- They are not registered or licensed in your state, check your state’s credit repair laws before engaging

- They make verbal promises that are not included in any written contract

If any of these apply to a company you’ve been speaking with, walk away immediately. You may also want to report them to the FTC at reportfraud.ftc.gov.

Credit Sweep vs. Legitimate Credit Repair: What’s the Difference?

Understanding the distinction between a credit sweep and genuine credit repair is critical to protecting yourself, and to making the right decision for your financial future.

| Factor | Fraudulent Credit Sweep | Legitimate Credit Repair (The Phenix Group) |

| What it disputes | Every item on your report, accurate or not | Only inaccurate, unverifiable, or outdated items |

| Legal standing | Typically illegal, violates FCRA and CROA | Fully compliant with FCRA, CROA, and TSR |

| Method used | False identity theft claims, forged police reports | Documented dispute process backed by attorneys |

| Results | Temporary at best, items return next billing cycle | Permanent when items are legitimately removed |

| Risk to you | Criminal exposure, FTC investigation, no refund | Zero legal risk, you are protected by consumer law |

| Timeline promises | 24-72 hours (a guaranteed red flag) | Honest, realistic timelines based on your situation |

| Cost structure | High upfront fees (illegal under CROA) | No upfront fees, fees after services delivered |

| What happens to debt | Debt is NOT erased, only reporting is temporarily affected | Inaccuracies removed; real debt addressed honestly |

What Actually Works: How to Legally Repair Your Credit

Legitimate credit repair is not about wiping your report clean, it’s about correcting what is wrong. Here’s what the process actually looks like:

Disputing Inaccurate Information

If your credit report contains errors, an account that isn’t yours, a payment marked late when it was on time, or a balance that is incorrect, you have the right to dispute it with the credit bureaus. This process is protected by the FCRA. Each bureau must investigate your dispute within 30 days and remove items they cannot verify.

This is time-consuming to do yourself. You need to contact each bureau separately, provide documentation, and follow up. One missed step can derail the entire process. That’s why working with a professional makes a measurable difference.

Goodwill Letters and Pay-for-Delete Agreements

In some cases, negative marks are accurate but you have context (a one-time late payment during a job loss, for example). A goodwill letter sent directly to the creditor asks them to remove the mark as a courtesy. Pay-for-delete agreements negotiate removal in exchange for settling an outstanding balance. Neither of these involves fraud, they are legitimate tools used by credit professionals.

How Attorney-Backed Credit Repair Accelerates Results

Most credit repair companies send generic dispute letters and wait. The Phenix Group takes a different approach. Our analysts work alongside a dedicated legal team that uses the same pre-litigation audit process that attorneys use, which forces creditors and bureaus to respond more quickly and completely.

When a bureau knows there’s a law firm behind the dispute, they take it more seriously. That’s why our clients see results that generic dispute mills simply cannot match.

Why The Phenix Group Is the Legitimate Alternative

We built The Phenix Group because we saw how many people were being failed — either by scammers promising magic fixes, or by legitimate companies that did just enough to keep collecting monthly fees. Learn more about The Phenix Group and our credit experts to understand how we operate differently.

Attorney-Engaged Process, Not Generic Dispute Letters

Every client program at The Phenix Group includes attorney oversight. This means our disputes carry legal weight that standard dispute letters do not. Creditors and bureaus cannot simply ignore or delay a response when they know attorneys are involved on your behalf.

Our credit repair pricing and process is transparent, no hidden fees, no long-term contracts you can’t exit. We believe in earning your trust every step of the way.

Custom Action Plans Built Around YOUR Goals

We do not send the same letter to everyone. After a thorough review of your credit reports from all three bureaus, Equifax, Experian, and TransUnion, our analysts build a plan specifically designed around your situation, your timeline, and your financial goals.

Whether you need to hit a credit score milestone before applying for a mortgage, resolve collections from a medical emergency, or remove errors left over from identity fraud, your plan looks different from everyone else’s, because your situation is different.

Real Clients, Real Results

Our clients have improved their scores by 100-150+ points within months, gone from denied mortgages to home closings, and saved tens of thousands of dollars in interest by achieving better loan terms. One client shared: after three months working with The Phenix Group, he had gained 150 points on his score and closed on his first home. Another described working with our team as similar to working with family, knowledgeable, attentive, and genuinely invested in the outcome.

How Poor Credit Affects Your Biggest Financial Goals

Whether you want to buy a home, refinance your current mortgage, secure a business loan, or simply stop paying sky-high interest rates, your credit score is the single biggest lever you have. See how we help home buyers get mortgage-ready and understand what’s actually at stake.

Consider this: a 1% difference in your mortgage interest rate on a $300,000 thirty-year loan means over $90,000 in additional payments over the life of that loan. Investing in legitimate credit repair now literally pays for itself, many times over.

We serve clients nationwide. Whether you’re looking for credit repair in Houston, TX, credit repair in Dallas, in Fort Worth, in Miami, or in New York City, our team has local experience and national reach.

Browse our service areas nationwide to find the team nearest you, or call us from anywhere in the country for a free analysis.

Frequently Asked Questions About Credit Sweep Services

Q: What is a credit sweep service?

A credit sweep service, in the credit repair fraud context, is when a company disputes every single item on your credit report at once, often by falsely claiming identity theft. This is typically illegal under the Fair Credit Reporting Act and the Credit Repair Organizations Act. A legitimate credit repair company will only dispute items that are inaccurate, unverifiable, or outdated.

Q: Is a credit sweep legal?

In most situations, no. A credit sweep is only technically legal if every single item on your credit report is genuinely fraudulent (such as in a documented identity theft case with a legitimate police report). For the average consumer, this is almost never the case. Attempting to dispute accurate negative items is considered fraud and can result in criminal charges.

Q: Can a credit sweep remove a bankruptcy from my credit report?

No. A legitimate bankruptcy cannot be removed from your credit report through any dispute process, credit sweep or otherwise. Bankruptcies remain on your report for 7 to 10 years depending on the type. Anyone promising to remove an accurate bankruptcy is lying and is likely running a scam.

Q: What is the difference between a credit sweep and legitimate credit repair?

Legitimate credit repair targets only inaccurate, outdated, or unverifiable information. It follows a documented dispute process backed by consumer protection laws, does not require false claims, and delivers permanent results when items are legally removed. A credit sweep disputes everything fraudulently, produces temporary or no results, and carries serious legal risks for the consumer.

Q: What should I do if someone offered me a credit sweep?

Do not engage. Do not sign anything or provide your personal information. If they have already taken money from you, report the company to the FTC at reportfraud.ftc.gov and to your state Attorney General’s office. Then contact a legitimate credit repair company like The Phenix Group for a free credit analysis to understand what can actually be done for your situation.

Q: How long does legitimate credit repair take?

Timelines vary based on the complexity of your credit file, the number of inaccuracies, and how quickly creditors and bureaus respond. Many clients begin seeing meaningful improvements within 3 to 6 months. The Phenix Group focuses on achieving results in the shortest honest timeline, not prolonging enrollment to maximize billing.

Q: Does The Phenix Group offer credit sweep services?

No, and this is a point of pride for us. The Phenix Group does not perform credit sweeps. What we offer is attorney-backed, fully compliant credit repair: a legal, strategic, and effective approach to identifying and removing inaccurate information from your credit report. We do not make promises we cannot keep, and we do not take shortcuts that put our clients at legal risk.

Q: How much does legitimate credit repair cost?

INTERNAL LINK NOTE [Editor: Link ‘credit repair pricing and process’ → /pricing/]

The cost of credit repair varies based on the complexity of your situation and the number of accounts that need to be addressed. The Phenix Group does not charge a flat subscription fee, our credit repair pricing and process is based on active work, with pricing determined after a free credit analysis. There are no upfront charges before services begin.

Ready to Repair Your Credit the Right Way?

You deserve a credit profile that accurately reflects your financial history, not one being held back by errors, outdated information, or fraudulent reporting. And you deserve a partner who is honest about what they can and cannot do for you.

The Phenix Group has helped thousands of clients across the country improve their credit scores through a compliant, attorney-engaged process. We do not promise overnight miracles. We promise expert analysis, personalized strategy, and relentless advocacy on your behalf, all within the bounds of the law.

Contact us today for your free credit analysis. No commitment. No upfront fees. Just an honest conversation about where your credit stands and what we can realistically do to help.